Consolidation, competition, and the cost of certification: Insight from New York’s AM Strategies 2024

Additive Manufacturing conferences rarely attract as many industry CEOs as New York's Additive Manufacturing Strategies event, let alone persuade them to share the stage for panel discussions. AMS2024 was no exception. On the back of a turbulent financial year for many of the industry's leading companies, how do those very CEOs see the state of the industry now, and what do they see as the biggest challenges ahead? Rachael Dalton-Taggart reports for Metal AM magazine. [First published in Metal AM Vol. 10 No. 1, Winter 2023 | 15 minute read | View on Issuu | Download PDF]

The seventh AM Strategies 2024 conference, organised by Additive Manufacturing Research and 3Dprint.com, was held in midtown Manhattan in New York City from February 6-8. This small but focused conference, with over a hundred speakers across three days, had a lot to offer. The focus, however, came down to three main topics: industry consolidation, what the industry is really in competition with, and the staggering cost of certification for Additive Manufacturing parts production.

With noticeably less hype from speakers than at many other conferences, and a seemingly genuine urge by key players to find ways for the industry to evolve, AM Strategies 2024 proved to be a unique event – and one to which I would like to return.

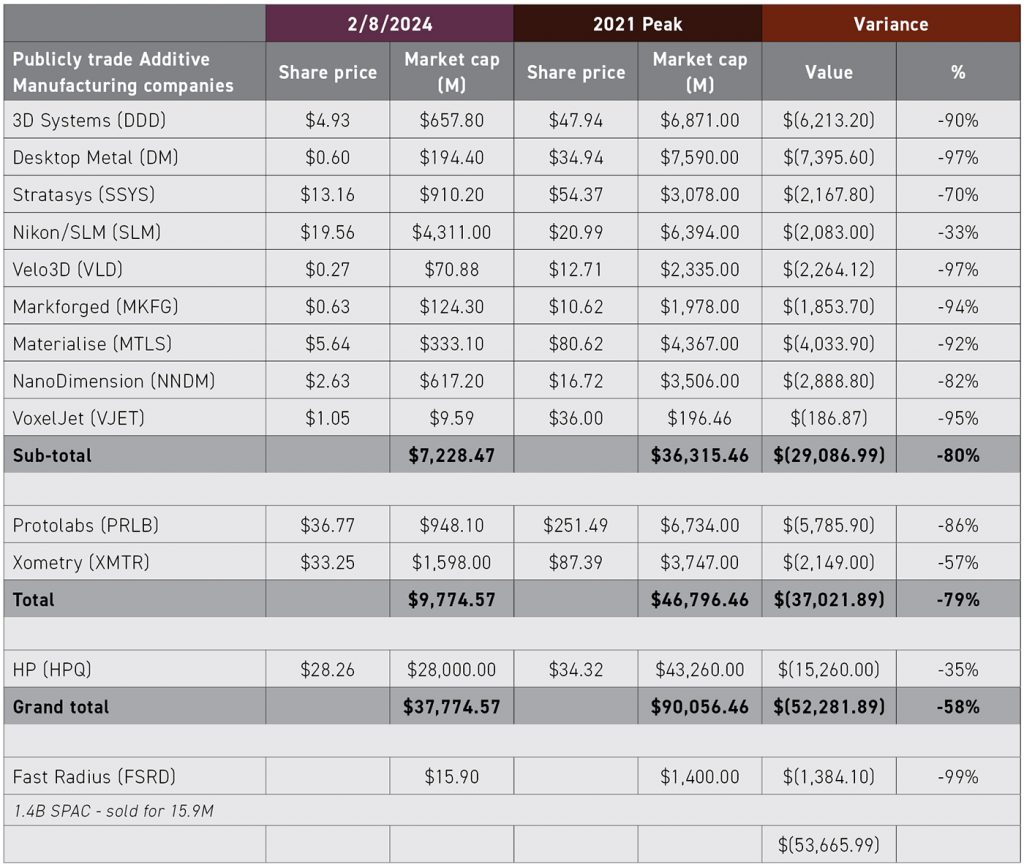

When considering the status of the AM industry, everyone acknowledges that it developed a financial wobble during 2023, with speakers attributing the Chapter 11 bankruptcy of Fast Radius – which had $200 million in investments – in 2022 and its ensuing fire-sale acquisition by Sybridge for $15.9 million, as the first warning sign. Indeed, industry analyst, Debbie Holton, pointed out to me during the conference that, since 2021, the total market capitalisation of the major Additive Manufacturing companies had dropped $54 billion in value since market highs in 2021, or an average of 80%, as of February 2024 (Table 1).

During 2023, the ongoing Stratasys saga – with Desktop Metal, Nano Dimension and 3D Systems levying bids – did nothing to boost confidence in the industry, with the months-long cycle of uncertainty and mud-slinging resulting in no mergers or acquisitions. Stock prices today remain noticeably low, and investors seem to be pausing. So, is this our new reality, or is the actual status of Additive Manufacturing better than the above suggests?

“Our industry is depressed,” said Asaid Yoav Zeif, CEO, Stratasys, during his keynote. “This cycle of stories [as described above] has caused people to lose confidence in the industry… but we are all still steadily growing. We will make it together. Our true competition is the status quo, and not within ourselves.”

Presenters agreed that growth continues despite investor caution. However, growth alone, among the individual companies, doesn’t solve the problems facing the industry. There are a lot of factors that need to evolve and be solved to ensure that market forecasts become a reality. “I am optimistic,” said Terry Wohlers of ASTM and The Wohlers Report. “But we have to be realistic and focus on the whole picture, which is good machines, good materials and not forgetting those very important workflows and proven applications.”

But even with the above in place, the situation in which many in the AM industry find themselves is far from simple. “The relentless focus on growth and revenue [for the financial markets] leads to a situation where companies are not focused on overhead and gross margins,” said Brad Kreger, interim CEO of Velo3D.

Scott Dunham, Executive Vice President of Research, Additive Manufacturing Research, stated, “The cost of money, interest rates, inflation, and government responses to global conflict will account for a lot of activity in the market. But we see that AM is competing more and more against traditional manufacturing and we have to focus on that.” Above all, Stratasys’s Zeif stated, “We need to be profitable. We then need to use that to scale and scope across technologies.”

Consolidation is key

The Additive Manufacturing landscape has become increasingly complex. It used to be a fairly simple industry, with just a couple of AM processes and just a few pioneering companies but, by 2015, there were so many new AM processes being commercialised that ISO/ASTM created and published the seven types of AM identified by the standard ISO/ASTM 52900:2015 ‘Additive Manufacturing – General Principles – Terminology.’

Over the past ten years, however, the number of AM vendors has mushroomed further, and AM ‘variants’ have been invented beyond the original seven. As a result, some fear that the landscape is becoming confused and largely unfocused. Reminiscent of the car-making industry, there are voices stating that consolidation has to occur. Many seemed to agree that a reformation – disintegration and consolidation – of the industry is needed to get into mainstream manufacturing.

“The ability to scale matters,” said Ric Fulop, co-founder & CEO, Desktop Metal. “But we don’t yet have a billion dollar AM company in the industry so consolidation is needed.” Yoav Zeif added, “We must join forces to consolidate like other complex and capital-intensive industries, creating the scale needed for manufacturing. Consolidating will enable higher R&D investment, establish complete ecosystems and workflows, allow greater standardisation, and create an internal network effect enabling delivery of solutions across global conglomerates.”

But no one seems to be too clear on how that consolidation would occur. Would a merger of two major Additive Manufacturing companies be approved by the SEC? Maybe greater collaboration – without merger and acquisition activity – would be beneficial if it was done sincerely.

Collaboration is already a key to advancing the industry through activities such as the 5550 Common Additive Manufacturing Qualification Template (CAM-QT), being led by America Makes and ASTRO America. This effort is focused on trying to understand and define the common requirements of AM qualification from key aerospace industry OEMs. It is reliant on collaboration from GE, Honeywell, and Pratt & Whitney, so that there is a common core for contractors to work to for qualification, with a view to reducing costs and time for future qualification.

Mario Dimovski, Director of Innovation and Transformation, Boyd Group, 3D in Auto Repair, explained during the AM for Mobility panel that collaboration is the key to the 3D Printing in Auto Repair Task Force, led by IBIS Global. This effort is designed to provide a secondary solution for OEMs or parts suppliers who might need smaller part runs that are more cost-effective than traditional manufacturing and additively manufactured in the region where there is demand. “In this case, experts have come together, including OEMs, to map out a regulated supply chain for ‘certified’ 3D printed automotive repair parts,” Dimovski stated. “Collaboration is a key to success in this.”

Certification and qualification: outdated?

Meeting certifications and qualifying machines, materials, parts and processes remain an expensive barrier to the more widespread adoption of AM – especially in metal. This is after achieving standard industry certifications such as ISO 9001 and quality standards such as SAE AS9100.

Indeed, there is serious concern in the US that arcane AM qualification requirements, especially in metals, mean that every machine, material, and part undergoes expensive test builds that are usually a cost to the parts supplier, not the purchaser. And this testing is not limited to the initial qualification stage either: testing has to continue throughout to ensure quality builds and any change of material or machine, even relocating a qualified machine requires requalification. “I talk to many metal AM producers and the big complaint is about the high cost of testing for qualification,” said Velo3D’s Kruger. “What are we able to do to reduce those costs?”

Additional testing requirements by prime contractors to the Department of Defence (DoD) mean that a Tier I/II supplier using metal AM for aerospace applications has to go through the standard requirements testing such as NASA 6030, then engage in testing for each different aerospace OEM. Therefore if a supplier wishes to provide parts to three different prime contractors, they have to run three different test build results, tuned to their proprietary requirements, thus increasing costs. With such high costs of entry, many potential suppliers will now not attempt to provide AM parts to the US aerospace and DoD supply chain – places where AM can deliver such high value.

“The cost of certification for users can typically exceed the value of the contract in hand, especially when the OEM only needs a limited amount of parts,” said AM Research’s Dunham. “We have to work with the government to create a funding line that will pay down the cost of certification. But the data created also has to be made available.”

The lack of available data for qualification is an area that can be solved through better software to manage the process, which will, in turn, provide better, more automated traceability.

But it was also interesting to hear the younger participants in the industry — all founders of more recent startups — deliver a verdict on current requirements. “We have to mythbust AM qualification and the outdated standards and requirements attached to it,” said Humna Kahn, CEO and founder, ASTRO Mechanical Testing Laboratory. This was amplified by Jonathan Cohen, CEO and founder, MIMO Technik, who stated, “Repeatability and reliability of the machines remains an issue. But while we are fixing that through machines, materials and software, we are still being held back by outdated standards and outdated thinking.”

However, such standards and requirements are driven by concerns about part integrity and human safety, especially for critical parts in flight or on and under the water. Matthew Sermon, Executive Director for Program Executive Office for Strategic Submarines, US Navy, explained, “We are not backing off on safety with AM parts for submarines in any way, but this is a national security imperative, and we will have to figure it out, and we will have to fundamentally change the way we do this.”

But no one can yet provide an answer for reducing testing and qualification costs. “The only way to reduce the cost of testing is to do less of it,” explained Harshil Goel, CEO of Dyndrite. This, by extension, means that test builds must be done faster, and there must be a higher degree of part success out of the gate. Goel contends that only new-generation software can achieve this – especially under current requirements.

New advanced software such as Dyndrite can provide significantly faster Design of Experiments, utilising and quickly testing hundreds of parameter settings (e.g. hatching, energy density, and thermal time) on a material and then building a recorded toolpath that can be repeated. This means test builds can be quickly refined programmatically, not manually, thus removing hours of manual 3D design and enabling quick resolution to ensure that a qualification build meets requirements. Recording these parameter sets means improved traceability and the ability to save and share the data with the right parties and other machines.

Many also believe the addition of Artificial Intelligence, or AI, can add power to that process. A start-up called AI Build promises to deliver intelligent tools that can scale AM processes through the automatic creation of workflows, supports, and toolpaths using process monitoring, thereby reducing build failures. But this still does not avoid the fact that each separate machine, material and part has to be qualified, regardless of model; that a software upgrade to a machine might not meet requirements and approval; and that requalification has to be performed.

Many companies, especially in metal AM, are working towards making qualification easier. Velo3D and IMI Global recently produced test results on the ability to build the same part, machine-to-machine, site-to-site without requalification. The key here is the ability to define and save build parameters and calibration instructions within the Velo3D equipment, replicate atmospheric conditions and produce consistent build quality. However, this does not bypass the current network of written requirements and qualifications specified by various associations or committees.

Time for the AM industry to grow up

AM companies have been competing amongst themselves to be recognised as leaders in this rather small, niche industry. A resounding theme through AM Strategies 2024 was the need to recognise the true competition: traditional manufacturing. To be part of this bigger picture, and compete with traditional manufacturing, the AM industry needs more reliable, repeatable applications.

“Market caps for AM companies were based on AM capturing the mainstream manufacturing markets,” said Dunham. “AM has been operating in a market that was parallel to traditional manufacturing. Now we have to compete fully against it.” EOS’s Gregory Hayes agreed, stating that, “We need to stop competing within our echo chamber. We should be focusing on supply chain and delivering repeatable and reliable solutions. We must focus on maturing the technology.”

Yoav Stern, CEO and Member of the Board, Nano Dimension, added, “Consolidation is now the only way to achieve a profitable business. The industry needs to grow up. Many AM companies built a business but failed to build a working business model. Your machine can’t move forward without fuel, unless it’s heading downhill.”

All attending seemed to agree that it is time for AM to grow up, focus on the bigger manufacturing picture and develop solutions that deliver positive use cases – and do it now, together.

After the dust has settled

AM Strategies 2024 was a fast-paced, intense conference. A lot was said, and many assertions made. There was even the faint promise of an industry that would work together more closely. But what does it all mean in the long run; what needs to be done?

Looking back at the event, Debbie Holton, manufacturing industry analyst and consultant and a moderator at the event, said, “I think of the Simon Sinek quote, ‘What got us here won’t get us there, and knowing who our worthy rivals are is the best way to help us adapt and improve before it’s too late.’ This obvious maturity gap in the industry shows a clear need for consolidation and collaboration, but we have to move toward boring rather than sexy applications, and all are signals of a needed change. Do we have a long-term enough view to see it that way? Or are near-term quarterly market-cap valuations making us too myopic?”

The clearest thing in the industry may be that the path to industry success is not clear at all. However, as Fulop put it, “2024 is going to be a make-or-break year for AM.” The need for profitability and rolling some of that profit back into R&D leads to the aim of consolidation of some of the bigger companies in the industry.

However, will historically competitive companies be able to cooperate, combine and collaborate in the spirit of ‘a rising tide lifts all boats’ (per John F Kennedy) as suggested through AM Strategies 2024? Or will it turn into a ‘last man standing’ scenario?

“Focusing on the proper ‘rival’ is one aspect of future success,” said Holton. “And the rest will require some mature, long-term industrial leadership perspectives and ‘ego-checking’ to truly industrialise AM. On my panel, Matt Sermon called it the ‘Manhattan Project’ for our time.”

Now what?

We have all heard the hype about AM over the years. Now we are hearing industry leaders pontificate about how to re-centre the industry and return to profit and much bigger revenues. But I remain cynical; after all, money talks, especially with the short-term focus on quarterly earnings. Will CEOs engage in more altruistic and meaningful mergers and collaborations in this year than in years past? Are their boards and investors willing to bet on long-term industry prosperity over more immediate company revenues? Can AM enterprises do this themselves, or do they need neutral direction by the non-profits like America Makes, BlueForge Alliance and ASTRO America?

Maybe at the next AM Strategies event we can start to hold them to account – report back what each company has done, sincerely, for the growth of the industry and not just for revenue streams. That is where the true value of this event will come to the fore.

Author

Rachael Dalton-Taggart

CEO, AshBridge Media Consulting, LLC

[email protected]

Rachael is a long-time veteran of the 3D technology industries, having reported and marketed MCAD, Reverse Engineering, and Metrology software, as well as traditional manufacturing and Additive Manufacturing technology. She now works as an industry researcher on projects designed to drive adoption and scaling of AM technologies into the supply chain.

LAST MONTH’S MOST-READ ARTICLES