A market analyst’s view: Europe’s opportunity as defence AM surges in the US and China

Drawing on insight from the AMPOWER Report 2025, this article examines how defence has become a key growth driver for metal Additive Manufacturing. While the US and China advance with coordinated, large-scale adoption, Europe risks falling behind. Matthias Schmidt-Lehr, Managing Partner at AMPOWER, offers a market analyst’s perspective on the strategic role of Additive Manufacturing in global defence, and what Europe must do to translate its industrial potential into meaningful defence capability. [First published in Metal AM Vol. 11 No. 2, Summer 2025 | 10 minute read | View on Issuu | Download PDF]

In a year marked by revenue declines and project delays across the Additive Manufacturing industry, defence emerged as a key driver of growth. According to the AMPOWER Report 2025, the global metal AM machine market saw a 3% revenue decline in 2024, despite an increase in units sold – a shift driven by falling average machine prices and mounting cost pressures on OEMs.

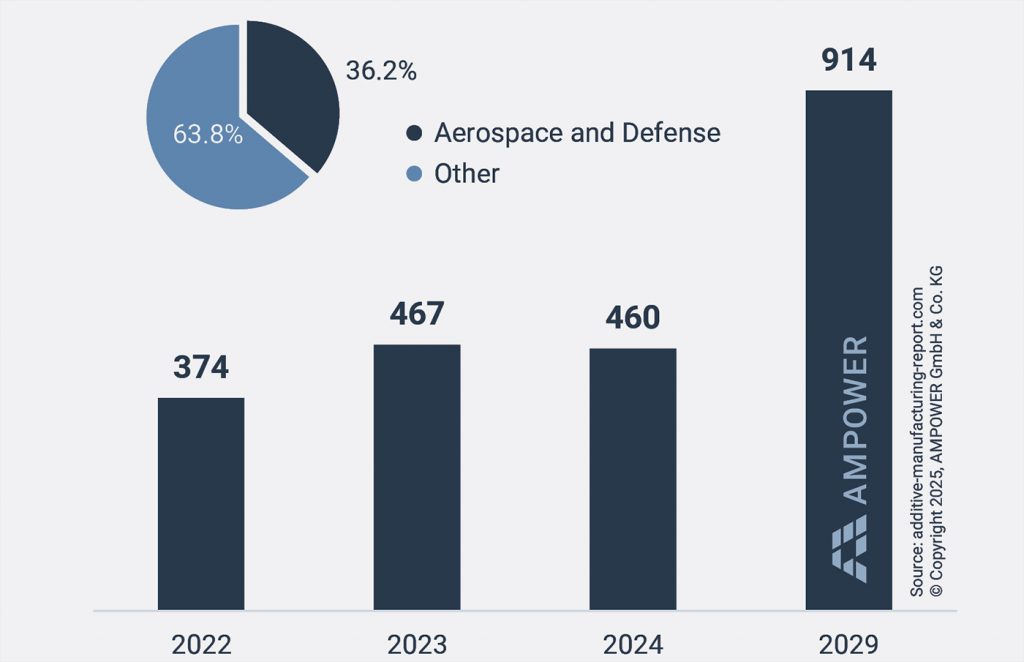

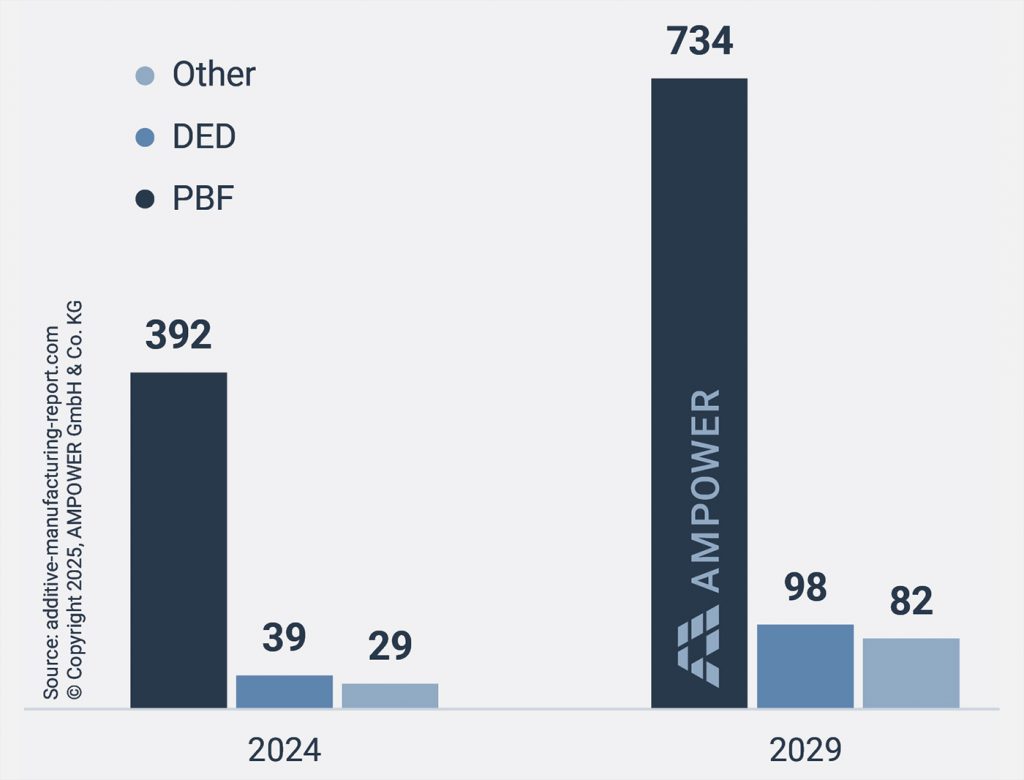

Against this backdrop, defence stood out as the fastest-growing vertical for metal AM machines, with equipment sales totalling €195 million – a year-on-year increase of more than 30%. Defence users now account for more than 15% of global metal AM equipment revenue and, when combined with the closely related aerospace sector, this figure rises to more than 36%.

This growth comes as conventionally strong sectors, such as medical and energy, have slowed. While industries like automotive and consumer electronics are beginning to explore high-volume production, broader momentum remains weak, with some companies reducing staff or scaling back their AM activities.

Amid this turbulence, defence adoption signals a shift in AM’s strategic relevance – not just as a tool for prototyping, but as a critical enabler of readiness, innovation, and logistics flexibility. Powder Bed Fusion (PBF) and Directed Energy Deposition (DED) remain the dominant technologies, particularly in aerospace and defence, where Europe continues to hold a strong OEM base, including Nikon SLM Solutions, EOS, and MX3D.

Global defence AM strategies: US and China surge ahead

Over the past decade metal Additive Manufacturing has evolved from an experimental tool into a strategic capability for the defence sector. Armed forces and contractors worldwide now use AM not only to sustain legacy systems but also to enable next-generation platforms such as hypersonic missiles and fighter aircraft.

The US: institutionalising AM at scale

In the US, defence-led procurement initiatives have driven a significant increase in AM adoption. The US Department of Defense has invested in PBF-LB and DED technologies in particular, fuelling a sharp year-on-year rise in both machine sales and consumables.

Metal AM plays a dual role in US defence strategy, supporting the readiness of current platforms and enabling innovation in future systems. The US Navy, for example, has institutionalised AM through its Additive Manufacturing Center of Excellence, developing digital part manufacturing data sets that will allow distributed production for submarines and surface ships. Replacing conventional casting with AM has cut lead times and supported the Navy’s ambitious submarine production goals, including Columbia- and Virginia-class vessels.

At the development frontier, companies such as Lockheed Martin and Raytheon have scaled AM integration into advanced hypersonic missile programmes, achieving cost and lead time reductions of over 90% for some components. AM is no longer confined to pilot projects but is embedded across operational supply chains and mission-critical production. Startups such as Beehive Industries are also innovating with AM-based propulsion systems, demonstrating how even small firms can contribute to agile, distributed supply chains within the US defence ecosystem.

The US model, with its coordinated infrastructure, digital qualification workflows, and public-private partnerships (such as America Makes), reflects a high level of organisational maturity.

China: accelerating AM through state-driven strategy

China’s military industrial complex has pursued a similarly ambitious trajectory, albeit through a more centralised, opaque model. Although less publicly documented, major military research institutes and state-owned enterprises such as China Aerospace Science and Industry Corporation (CASIC) and AVIC have embedded AM into production lines for cruise missiles, UAVs, and advanced fighter aircraft.

For example, CASIC uses AM to produce components such as rudders and engine housings that were once reliant on casting and welding. These parts are now made in days, with reduced waste, fewer personnel, and improved performance through optimised geometries. Shenyang Aircraft Corporation has integrated AM into the manufacturing of aircraft – likely including the FC31 stealth fighter – with reports indicating significant use of AM for structural components that reduce weight while enhancing strength.

China’s approach to AM in defence is both assertive and strategically aligned with its broader goal of military-technological self-reliance. AM is used to bypass traditional manufacturing bottlenecks and reduce dependence on foreign suppliers, enabling faster deployment of advanced capabilities.

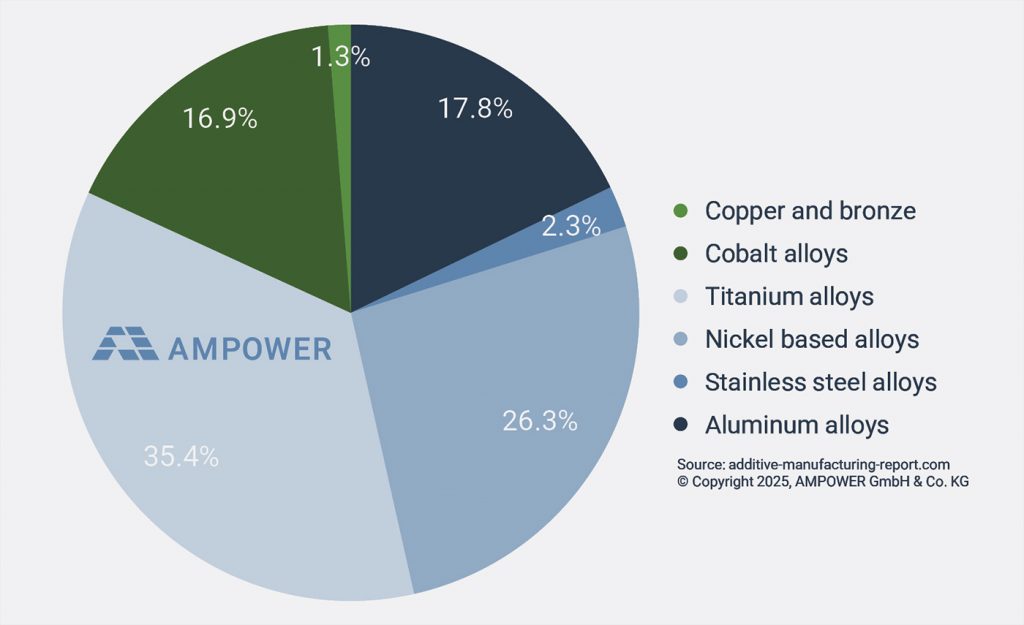

Material use in defence also reflects this strategic divergence. Aerospace and defence applications have a strong focus on high-value alloys such as titanium, nickel, and cobalt – materials that support weight reduction, strength, and performance under extreme conditions. In contrast, stainless steel, which accounts for nearly 17% of global AM powder demand across all sectors, makes up just 2% of material usage in these applications (Fig. 5). In China, this emphasis on high-performance alloys supports its drive to develop propulsion systems, airframes, and thermal shielding for next-generation platforms.

Europe’s defence AM momentum: catching up or falling behind?

Because of their global operations, many leading AM companies do not routinely segment industry sales data by market within specific regions. As a result, no definitive data confirms that aerospace and defence companies in Europe invest less in AM compared with the US or China. However, most machine OEMs interviewed for the AMPOWER Report 2025 indicated that aerospace and defence spending in the US and China drove the majority of their growth in 2023 and 2024, whereas similar momentum has yet to materialise in Europe.

This is supported by numerous public announcements from machine OEMs, component manufacturers and materials suppliers, as well as public funding bodies such as the US Department of Defense. The volume of announcements from defence primes and their suppliers further suggests that AM activity, particularly in the US, has been growing significantly faster than in any other region globally.

Europe does have some promising activity in the defence AM space. The UK Ministry of Defence deployed Cold Spray AM systems during NATO’s Steadfast Defender exercise. MBDA Systems has developed missile components using AM. Rolls-Royce is recycling titanium from decommissioned Tornado aircraft to print parts for the next-generation Orpheus engine under the Future Combat Air System (FCAS) programme.

However, these remain isolated rather than integrated into a broader ecosystem. Europe lacks a unified strategy for defence-related AM. Its industrial base is scattered across national borders and hampered by complex procurement systems and constrained budgets. Although companies such as Airbus Defence, Rheinmetall, and EOS have shown AM leadership, overall momentum is limited by a conservative innovation culture and risk-averse decision-making.

AM in Europe is still too often viewed as a sustainability experiment or digital pilot project rather than a scalable production technology. There is little evidence of the kind of strategic coordination seen in the US or China – between defence ministries, OEMs, and AM technology providers.

Can Europe catch up?

The US has taken a deliberate and highly coordinated approach to integrating AM across its defence ecosystem. Metal AM is now embedded in both sustainment and innovation pipelines, enabled by strategic infrastructure, digital qualification processes, and public-private initiatives. This has positioned the US as a global leader in the defence adoption of AM, with results already visible in both operational readiness and platform development.

China’s approach to AM in defence is equally assertive but structurally different. It follows a model of state-driven acceleration through tightly integrated government industrial complexes. Reports indicate that AM is widely used for engine components and large airframe structures across advanced military platforms. While transparency is lower than in the West, it is clear that China seeks to bypass conventional bottlenecks, reduce foreign dependence, and gain a leapfrogging advantage in military technologies. China’s emphasis on vertical integration and self-reliance is evident across both prototyping and final part production.

By contrast, Europe’s adoption of AM in defence remains cautious and disjointed. While promising efforts exist, these remain the exception rather than the rule. Without a cohesive industrial strategy and cross-border alignment, Europe risks falling behind in critical areas such as hypersonics, logistics agility, and digital part certification.

To stay competitive, Europe must shift from pilot projects to full platform integration. It should align procurement and certification processes to support AM and encourage cross-border collaboration. Without this shift, Europe could become strategically dependent on others for next-generation defence readiness.

Realising AM’s potential in European defence

Despite these challenges, recent geopolitical events have led to a rise in European defence spending. Tensions in Eastern Europe and the Middle East have prompted EU member states to increase defence budgets for 2025 and beyond. The European Defense Fund has allocated new multinational grants to support collaborative research in advanced manufacturing, including metal AM.

These developments show that defence spending is shifting toward digital and lightweight manufacturing, with metal AM positioned to benefit. As member states expand budgets, AM will capture a larger share of defence allocations, boosting demand for machines, feedstock, and software. European armies face a similar challenge to US forces, with ageing fleets and difficulties in the supply of spare parts.

Strategically, higher defence budgets may accelerate the harmonisation of AM certification across Europe. Under the European Defense Agency, member states could adopt a unified Directive for AM Qualification. This would streamline collaboration and reduce barriers to entry for smaller OEMs. Such efforts could lead to a European Defense AM Consortium – promoting best practices, strengthening supply chain security, and enhancing the resilience of Europe’s defence capabilities.

The broader economic impact will extend beyond defence. Innovations in alloys and certification from defence programmes will benefit civil aerospace and green energy. Stronger regional collaboration will improve supply chain resilience. In short, if Europe aligns its strategy with execution, it can narrow the gap with the US and China and reclaim a leadership role in AM for defence.

Europe already has a strong industrial base to build on. It is home to leading equipment OEMs such as Nikon SLM Solutions, EOS, and MX3D, which are at the forefront of Powder Bed Fusion and Directed Energy Deposition technologies. From a supply chain perspective, the capability to support defence programmes is already in place – what’s needed now is strategic coordination and political will to fully activate it.

Author

Matthias Schmidt-Lehr

Managing Partner

AMPOWER GmbH & Co KG

additive-manufacturing-report.com

The AMPOWER Report 2025 draws on insights from over 300 in-depth interviews with Additive Manufacturing managers and directors, offering a balanced view of both technical and commercial trends.

This year’s data set includes more than 44,000 individual data points, with equipment OEMs representing around 90% of the global installed base. In addition to capturing supplier perspectives, the report places particular emphasis on user feedback, enabling a demand-driven evaluation of the market.

Complementing the data, a series of guest-authored articles explores regional developments across the global AM landscape.

LAST MONTH’S MOST-READ ARTICLES