Current perspectives on metal AM: Hype, volume manufacturing and the geographies of production

Metal AM exists in a potentially confusing place between the world of 3D printing and its ‘maker’ movement, and Industry 4.0, with its drive towards new economic models. Here, Dr Jennifer Johns, Reader in International Business at the University of Bristol, UK, contextualises metal AM within broader narratives around technological change and economic development, Industry 4.0 and the Factory of the Future to give us a better understanding of what the outside world expects. Drawing on recent empirical research, different and often contradictory viewpoints are presented on the key issues facing the move to volume manufacturing and the geographies of production. [First published in Metal AM Vol. 6 No. 1, Spring 2020 | 30 minute read | View on Issuu | Download PDF]

Recent years have seen consistent media and industry interest in Additive Manufacturing, fuelled by reports of high growth rates and publicity around exciting new case studies. The ‘hype’ surrounding AM has increased the external profile of the industry but has also resulted in some damaging consequences. One such consequence is the lack of realistic approaches to understanding the sector and the degree to which it can ever be as transformative as pundits would lead the general public to believe. This article does two things. Firstly, it contextualises metal AM within broader narratives around technological change and economic development, ‘Industry 4.0’ and the ‘Factory of the Future’, to give us a better understanding of what the outside world is expecting of the technology. Secondly, it pays close attention to two of the most significant areas of projected change – the volume and geographies of production – and draws on recent empirical research to present different, often contradictory viewpoints. This will offer insight into how well metal AM industry insiders feel it is able to meet external demands. The focus of this article is predominately on Laser/Electron Beam Powder Bed Fusion (L-/EB-PBF), as these are the most mature metal AM processes and currently offer the highest level of technological readiness. Other technologies, such as metal Binder Jetting, are highlighted where interviewees raised them as presenting a potential deviation from the development trajectories of L-/EB-PBF. The article will conclude with some reflections on the evolution of metal AM and on the possible outcomes of the dialogue between those inside the industry and those outside it.

For many external to the metal AM sector, it is included under the non-specific umbrella of ‘3D printing’, and as such is more strongly associated with the ‘Maker Movement’ and ‘Makerspaces’ and their ubiquitous plastic chess sets and 3DBenchies. The diversity of different technologies, materials and applications that make up the world of Additive Manufacturing, and metal AM specifically, is not widely acknowledged. Nor is the scope of metal AM in industry (either as a prototyping or a production tool) widely understood. Instead, in the public – and often policy-making – imagination, 3D printing forms part of the vaguely understood Industry 4.0, as a tool of the ‘Factory of the Future’.

As a consequence, the value and future trajectory of metal AM is bound up with the narrative of a wide number of different kinds of technological progress, including AI and big data. For those within the metal AM industry, who certainly view AM as having a significant role in the Factory of the Future, this can obscure the identification of the change dynamics and particular industry and policy demands of the sector.

The current rhetoric around Industry 4.0 is driving many national government strategies around technology in manufacturing and the move towards full automation of production lines and factories. In 2019, the World Economic Forum met in Davos, Switzerland, to discuss ‘Globalisation 4.0: Shaping a Global Architecture in the Age of the Fourth Industrial Revolution’. The agenda considered how countries can respond to, and shape, changes in how goods are produced, distributed and consumed. This is based on the idea that the world is entering a fourth industrial revolution, where a wave of technological progress will launch us into a new era of globalisation. The world’s leaders are pinning their hopes for economic growth on technological leaps, of which AM is expected to be one. These global discussions are mirrored by national initiatives such as the widely-mimicked German Industry 4.0 strategy, the UK’s Industrial Strategy and Chinese action plans around technology development.

Pressure and expectation are weighing on the AM sector as a whole to make progress in machine capacity and speed, integration with other technologies and processes such as robotics, AI and big data, and to transform supply chains to increase speed of delivery, often through localised distributive manufacturing. Unpicking the role of metal AM is unclear, as ‘3D printing machines’ are perceived as multi-material (plastics, metals and electronics) and multi-functional in this narrative. With global economic growth continuing to falter and no easy solutions apparent, the weight of expectation is likely to increase, not decrease, and delivery is expected to be in terms of years, not decades. Much is being asked of AM.

These expectations are amplified by academic work on AM. While engineering and material sciences focus on technological advances, social science has begun to focus on what it still calls 3D printing. Sociologists, economists, management scientists, geographers and political scientists have been musing over the societal impacts of 3D printing, focusing on predictions of a narrowing of the gap between producer and consumer as individuals design and print their own consumer goods. This work has offered valuable insights into how 3D printing could transform production and consumption. Supply chain management has begun to model scenarios around the length of supply chains based on known variables related to different configurations of machines, their capacity and proximity to suppliers and customers. One of the most significant papers written in my field of international business makes a series of predictions about the impact of AM in manufacturing and suggests which sectors will be most likely to experience transformative change. It is, unfortunately, based on several misconceptions of the sector, the result of information sourced from secondary industry and media reports, and fails even to distinguish between technologies and materials.

In consequence, I secured funding from the British Academy to spend time talking to the AM sector, interviewing owners and senior management in AM firms and their OEM users in the UK, US and Germany. Between 2017 and 2019 I interviewed fifty-two individuals from across the supply chain about their operations and business strategies, and what they saw as the current and future directions for AM evolution. Around half of the interviewees worked in, or in roles connected to, metal AM (e.g. metal powder suppliers), and all interviewees spoke to the whole AM sector. I attended the global industry conference at Formnext, Frankfurt, Germany, in 2017 and 2018, and presented my initial research findings at the Additive Manufacturing User Group (AMUG) Conference in Chicago in 2019, where I will present again in March 2020. The rich interview dataset available to me reveals many interesting findings related to the changes within this sector, including common challenges and barriers, underlying business models, regulation and standards, policy-making and innovation rates, as well as a wealth of historical information on the evolution of the AM industry. This article will focus on two current and topical debates. First, that of volume Additive Manufacturing and second, the reshoring of production.

Metal AM: From prototyping to volume manufacturing?

For several decades, AM has been used primarily for prototyping, across all industry sectors. “We had technologies that were OK for prototyping parts but not for functional parts,” stated one of my interviewees. A common source of commentary and debate within the sector – demonstrated by my research and also the programme content of conferences such as Formnext and AMUG – is the issue of how the industry can increase its production of functional parts and achieve manufacturing in larger volumes. A source of intense debate is how close AM is to high-volume, functional part production. This discussion will focus on some general trends and specific issues related to metal AM and place the debate within the context of Industry 4.0 and the Factory of the Future.

From prototyping to manufacturing

The process of moving to parts for end-use applications is not straightforward, and the sector’s long association with prototyping has created some challenges. “The prototyping applications of technology have a very long background. They’ve got excellent diffusion in the manufacturing industry; everyone’s aware of it, everyone uses it for that, and that’s fine,” explained one interviewee. “Proposing this for manufacturing, the story changes a little bit, and in many companies who use it for prototyping, they wouldn’t even consider using it for manufacturing, simply because of the associated experience with the technology.” Despite the hype around AM, within industry there remains a perception barrier to overcome. This is due to the increased demands being placed on the technology. “There have been some stories out there with folks who have struggled for way too long simply because they didn’t get the proper training or the decisions with choice of materials versus process. It is taxing to get to the application you are looking to. Going to production puts a spin on that because our expectations are much higher than with prototyping. You can make a prototype that is pretty strong, but if you make a production part it has to work,” they added.

Speed

Among my sources, opinions diverged on the importance of speed in Additive Manufacturing, with a consensus that current build speeds are no longer a significant barrier to adoption. Laser/Electron Beam Powder Bed Fusion parts often have long build times, but other factors such as functionality were considered relatively more important, along with total product development time. “We’d always take more speed. It does, however, also have to perform. So, if it is a trade-off against functionality, then no, we wouldn’t take it. No, we wouldn’t take it ever. Whatever it is doing, it has to perform,” one source commented. Build speeds have to be considered as part of the whole production process. “When you include the set-up time, 3D printing can be much, much faster than other methods. So speed is something that all of the 3D printer vendors are working to improve, but even so, 3D printing has its place when you talk about speed.” A broader perspective, then, needs to be adopted when making manufacturing decisions.

Production volumes

Recently, the focus has been on whether metal AM can meet the demands of industrial production. There is some disagreement about whether this is happening now, is a short- to medium-term possibility, or remains a future goal. “To happen on an industrial scale, we need to see serial manufacture. One part may be made at volumes of say 10,000 a year. This is becoming a possibility,” one source stated. However, there are sectoral differences, and it is currently easier to ‘sell’ the business model for smaller parts. “A lot of our repeat production customers are producing relatively small things in quite high numbers.”

Several interviewees expressed confusion around what the industry meant by ‘volume’; i.e hundreds, thousands or millions. Aerospace and Formula 1 are heralded as leading the adoption of AM, due to their comparatively low volumes but real-world use of the technology. The leap to industrial-scale manufacturing in other sectors familiar with AM prototyping will be harder. “The automotive industry is a high cost pressure industry, so they need low unit costs and high volumes, and it’s not really a thing that additive is good at, at least at the moment,” one source noted.

Indeed, many felt that the industry needed to be more conservative about both its claims for current and future capacities. “We’re not at high volume,” stated one interviewee. “It can be a few hundred a year or it can be several thousand. I think the highest volume we will see is about 75,000 a year, but a lot of things will just be thousands, not tens of thousands.” The race to high volumes also risks overlooking potential areas for growth. “We’re getting there in the transformation from small volume to high volume, but I think the small-volume market is one of the markets that’s underestimated. So everyone is looking at the high-volume application, for example, the eyewear or shoe sole industry where you get millions of parts a year, but actually what makes the biggest amount when you look at our revenue or the revenue that our customers do, it’s more serious, and that’s 50 to 500 parts or something, and there are many applications out there.”

Metal AM technologies

Conversations about the type of metal AM process that will achieve industrial scale manufacturing highlighted the fact that there isn’t a single trajectory of development. “The most advanced technologies in the industrial context are powder bed with their selective laser sintering processes,” stated one interviewee, reflecting the wider global focus on L-PBF AM. However, sources repeatedly acknowledged that there are alternative technologies becoming more viable. One global OEM stated that it has been holding back on investing heavily in a single technology, instead preferring to observe competitors and wait for alternative technologies to mature. “They [competitor OEMs] have invested in powder bed laser fusion equipment and been playing on it for some years. It is all very good as learning, but the probability is that it won’t be powder bed laser fusion techniques that drive the price point down to a point at which our industry can seriously look at making metal laser fused end-use components.”

Binder Jetting processes are viewed as having significant potential in moving metal AM towards industrial production. “There are opportunities with some of these new binder jet processes coming out. As the metals industry leverages the Metal Injection Moulding industry, I think there will be opportunities to leverage metal parts at a much lower cost and maybe a higher throughput,” one stated. However, the suitability of these new technologies varies depending on function. “The main issue in the Powder Bed Fusion process is the internal stresses. So it will have its uses whether you build multiple components or whether you start using different hybrid processes, [Binder Jetting could be the] perfect technology for particular types of components, not for us, not for very complex thin walls, thin wall heat exchangers, but for other components I see it as a way forward, because of the build rate and the post-production. At the moment the Powder Bed Fusion process helps us realise our design. The design is the driver rather than the technology.”

Business models

Progress is being made in AM in relation to the break-even point in comparison to traditional manufacturing methods. As one source reflected, “Clearly 3D printing is more attractive for smaller runs of parts in terms of number of units, and other methods are more attractive to larger volumes. So the question is where the break-even between those two happens, and that’s a matter of some debate. The break-even is very different, depending on what exactly it is that you’re fabricating.” Speed is not therefore independent of other variables. Significantly, though, there are several indicators that a wider perspective needs to be taken on the value of metal AM rather than cost per part. The potential time savings, as suggested above, due to process and/or reduced logistics and also a wider concept of value. This includes consideration of the whole lifetime of the part as considerable cost savings may be made through the use of AM. The use of metal AM in building functional parts for aircraft due to weight savings is an obvious example. Greater strength and durability of products may also be a significant factor due to sustainability agendas. Vertical integration can allow the whole production chain to be viewed in full. “The value chain can be optimised and costs manipulated. The discrete bits of tech all add up. You can then drive the economics of it. You can get costs down and quality up which means that serial manufacture comes onto the agenda. This helps to overcome the overriding perception of AM as low volume and for prototyping.”

Many discussions of industrial manufacturing noted the shift of focus from polymer AM to an acknowledgement of the potential of metal AM at the industrial scale. “There is a much greater history of people using additive on the polymer side so what we are seeing is an increase in metal additive both in the volume and in the criticality of the parts that are being pursued,” stated one interviewee on the topic. Awareness that ‘there are critical parts flying now’ is leading to renewed confidence in the capacity of metal AM in industrial production.

‘Selling’ the business model

The sector is keen to emphasis the potential of AM and to publicise the advantages that AM offers. As one source put it: “Higher productivity, better economics, lower waste. It’s really hard to see anything wrong with it; it basically delivers on all fronts.” Part of this process, which relates back to the race to high volume, contexualised within conventional understandings of how products should be designed and manufactured, is emphasising that more systemic change needs to happen. “Which I think is the crucial difference with AM, isn’t it?” they stated. “That’s what the selling point is, it’s actually we’re not saying we can do existing things better, we’re saying we can do totally different things. And proving that there’s a business model underlying it.”

Two things need to happen in relation to how the metal AM business model is understood within the industry and externally. First, there needs to be greater transparency around existing business models. Many expressed extreme frustration at business models that were marketed as successful but which were increasingly questioned as unfeasible and pushed to drive market growth and the profile of particular AM firms. Second, the tendency to view metal AM (and AM in general) as a unique and special technology may be alienating potential users and limiting application. “We think the A-list celebrity status of AM needs to be normalised,” one company stated. Part of my research examined the rhetoric around the replacement of conventional technologies by AM. This is not voiced at all within the industry, where there is instead widespread acknowledgement that metal AM is one tool among many, sitting in complement to established production processes.

Barriers to higher volume manufacturing

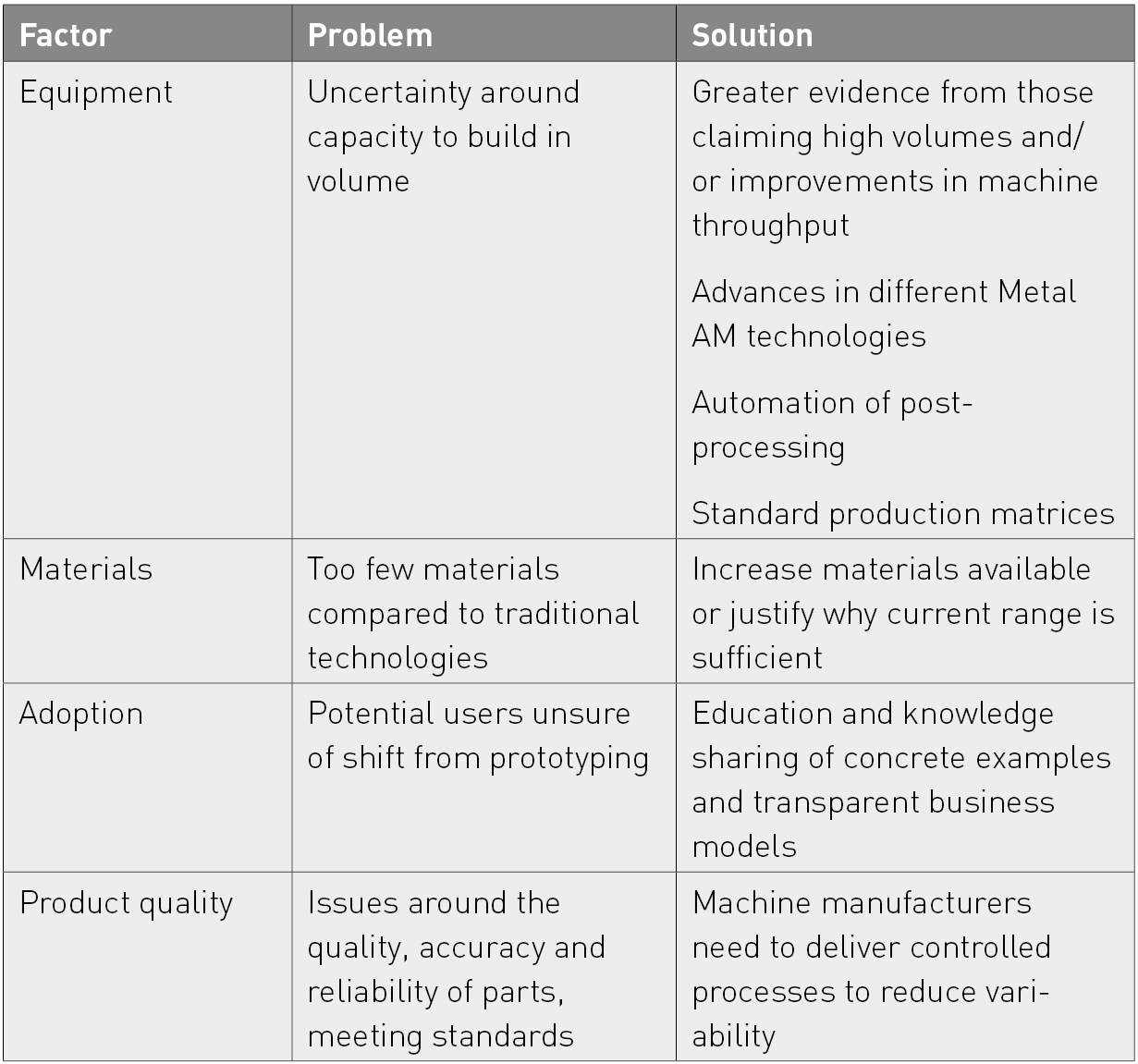

There are numerous issues for metal AM to tackle with regard to the shift away from prototyping. Table 1 outlines the four key factors. A firmly-voiced concern of several OEM users was on the current capacity of metal AM machines. “Many of the machines around us are not really production capable. They are good for prototyping, they can be improved for niche applications, but as volume manufacturing equipment they aren’t there. What we need are lower cost, faster, scalable platforms that can work with a variety of materials,” stated one OEM. Others had a different vision of how machines could be configured to produce the required outputs: “I believe the future is not necessarily a large machine that is very expensive; as long as you can print a part in a given build volume it’s better for companies to consider multiple machines so they can have true flexible manufacturing and scale.”

To summarise, there are divergent opinions on how far metal AM has come in the shift from prototyping to volume manufacturing, from extreme scepticism of the claims that volume production is occurring through to enthusiastic certainty. Much insight can be gained by stepping back from our examination of the technology and price-per-part to consider the broader rationale for using AM. A key necessity is greater transparency around the business models underpinning higher volume AM production. Currently, publicised examples are treated with a level of distrust by industry, and this results in a more uncertain and confusing environment for potential adopters.

Geographies of production

In addition to the focus on production methods, AM is expected by the general public, policy-makers and many in academia to not only transform how products are made, but also where they are made. The technology has the potential to radically change the geographies of where products are designed, prototyped, produced and distributed by radically reducing supply chain length and delivery times.

Reshoring is the process of bringing offshore operations back to their originating country. It is viewed as a contemporary counter-balance to the new international division of labour caused by the acceleration of globalisation since the 1970s. This caused a wholesale shift in manufacturing to low-labour-cost economies in the Far East. More recently, the rising cost of labour in developing countries (including China), peaks in oil prices, increased transport costs and supply chain vulnerabilities have resulted in some evidence of a shift back to advanced economies such as the US and Europe. Firms are also driven toward reshoring by the economic downturn, sustainability agendas, customer demands for flexibility and pressure to improve cost performance to consider where to undertake all parts of their production process.

The phenomenon of reshoring has gained greater prominence due to political engagement with the topic. In the US, it became a campaign issue during the last presidential election, with Donald Trump stating that he wants to see more manufacturing on American soil. In the UK, it has been cited as a possible solution to the negative economic and trade consequences of Brexit. The Economist recently cited the Chartered Institute of Procurement and Supply (CIPS) as their survey suggested that almost a third of British businesses that use EU-based suppliers were seeking British replacements.

AM is intimately tied up in this narrative, as the technology appears to offer a high-tech solution to the problem of severed international supply chains caused by political actions and/or firm-based strategies. During my conversations with those in the industry, the vast majority expressed scepticism about the degree of contemporary evidence of geographical shifts in production. However, a few anecdotal references were made to the return of some forms of prototyping and some injection moulding (both due to speed and quality issues) from China to the US, Germany and UK. Many in the industry also articulated strong opinions around how they envisioned the future of production and metal AM, positing several different interrelated factors as outlined below.

Dominance of traditional production methods

Rather than seeing AM as a factor in reshoring, several interviewees cited change in existing conventional supply chains as being due to concerns around quality and delivery times. “I already have some customers that are bringing it back from China because of problems they had with the supply chain around delivery uncertainty and poor quality,” stated one. Other more strategic reasons were also cited. “A lot of it is to do with the tax laws. A big corporation relocated here [to the US] to take advantage of tax loops. They are playing that game in Ireland too.”

These interviewees saw little or no role for AM in the short-term in driving geographical changes in supply chains. This was due in part to the dominance of existing supply chains by conventional production processes; metal AM has insufficient power to drive those changes while it is dwarfed by other technologies. “Even in a single site, never mind multiple sites, doing diagnostics of the processes because I am using additive, I still at the moment have to use traditional supply chains for most parts,” one interviewee explained. “The ability to change a design within a few moments and then make a part within hours is significant. You can’t do that sourcing from Asia.” This was also due to the fact that metal AM parts often form only a small part of a final product, again diminishing the capacity for change.

Design for AM

The transformative potential of metal AM is being curtailed by contemporary limitations on designing for AM. “The transition for designing for additive hasn’t really been established. Once parts are optimised for additive then location for manufacturing is almost meaningless,” stated one company’s CEO. This interviewee saw potential for significant change, but this is predicated on systemic shifts in how production parts are designed and manufactured. The decision to use metal AM parts needs to happen at the design stage to maximise the benefits of using AM. This too can influence where the actual production takes place. As labour costs rise in developing countries, decision-making around which parts of the production chain drive location decisions may alter. “The cost of manufacturing, the cost of an AM machine is the same in China as it is in the UK, to cost the material is the same in China as in the UK, so in that respect it levels the playing field,” they stated. “So if that means that the design holder, the person that’s commissioning that work, is based in the UK, then yes, it is more likely to come over to the UK.” This adds significant complexity in a still largely vertically disintegrated industry around the locational demands of the various parts of the production process, from design through to distribution.

Labour costs

The majority of interviewees understood the location of production based on the analysis of costs, with the primary factor being labour costs. There was, however, tension between opinions on the impact of increased automation resulting in reduced labour costs. Many in the industry aligned themselves with the political discourses around AM leading to reshoring to advanced economies, arguing that reduced labour costs would make production more feasible in ‘home’ markets. This argument is based on the understanding that more advanced, high-tech technologies do tend to stay closer to their home markets, or lead firms. The vast majority of global firms retain their core research and development facilities in their home markets, often close to their headquarters. There are good strategic reasons for this related to the protection of IP, recruitment of skilled labour and inter-firm interaction, which are eased through greater geographical proximity.

Relatedly, the home markets are those that seek, and are prepared to pay for, cutting-edge technologies. “In the Far East, the demand isn’t necessarily for the expensive multi-laser, process monitoring machines, it is much more for the cheap machine and of course there are a number of Chinese manufacturers who have copied machines or invented their own machines. The latest technology tends to be consumed in the advanced economies,” stated a source. Similarly, metal AM machines are still far from being ‘plug and play’, demanding trained operators and maintenance which are all presently easier to access in advanced economies.

However, two counterpoints were offered to this position regarding labour costs. The first is the present-day limitation regarding the relatively high degree of manual labour involved in metal AM, including post-processing. This is a barrier to full automation and sufficient reduction of manual labour to trigger the recalculation of costs in different geographical locations. “As long as there is a lot of assembly needed, which is labour intensive, then it will basically stay in the countries where they stay. Once you remove the manual assembly work, then for sure the production can go where the parts are needed or where the products are sold.”

The second is that, over time, labour costs will again become more significant, creating subsequent drivers towards lower cost locations. “At the moment, the throughput and cost-per-part and the technology is such that the labour cost isn’t really the issue,” a source noted. “However, as we increase the throughput and as we bring down the cost-per-part, then I am sure the labour rates will become more of an issue and then the machines will probably be taken up more widely in those markets where you get that advantage.” This is predicated on significant advances in the metal AM machines, and on support infrastructure. Therefore, this is likely to first occur within OEM organisational structures, i.e metal AM production sent to subsidiaries in developing countries rather than through outsourcing agreements.

Sectoral and volume variation

Interviewees felt that small, low-volume series of production are the most likely to reshore and suggested that the current limitations around the scale of production, as discussed above, are limiting the potential for a significant shift in global supply chains. As one interviewee explained, “In terms of high-volume production, we haven’t seen any evidence so far where someone is taking high-volume production from China, moving it to the US or Europe, and saying ‘because we can do this with 3D printing, now we’re moving it back,’ because high-volume manufacturing in China is increasingly automated itself and so the difference in what you can achieve in terms of labour costs between China and the US is shrinking. So I don’t see 3D printing just completely transforming the economics of manufacturing high-volume products overseas.”

There is a high degree of sectoral variation. Aerospace firms in the US pointed out that they have been prevented from offshoring by government regulations. There are, however, some widely-cited sectors in which we can observe some reshoring. “AM has the potential to change where things are manufactured, and maybe it depends on the applications… for sure, all our eyewear customers produce in Europe. None of them produces the glasses in China or Asia. Would they have done in the past? They have done in the past, but only the low-quality frames,” stated a source. Similarly, the relocalisation of dental implant and related production has seen significant shifts over recent years, with dentists able to build implants in their own dental surgeries rather than subcontracting production to centralised labs. If they do subcontract, it is more likely to be to an AM service bureau, although it should be noted that dental implants never tended to be sourced using geographically extensive supply chains due to time demands.

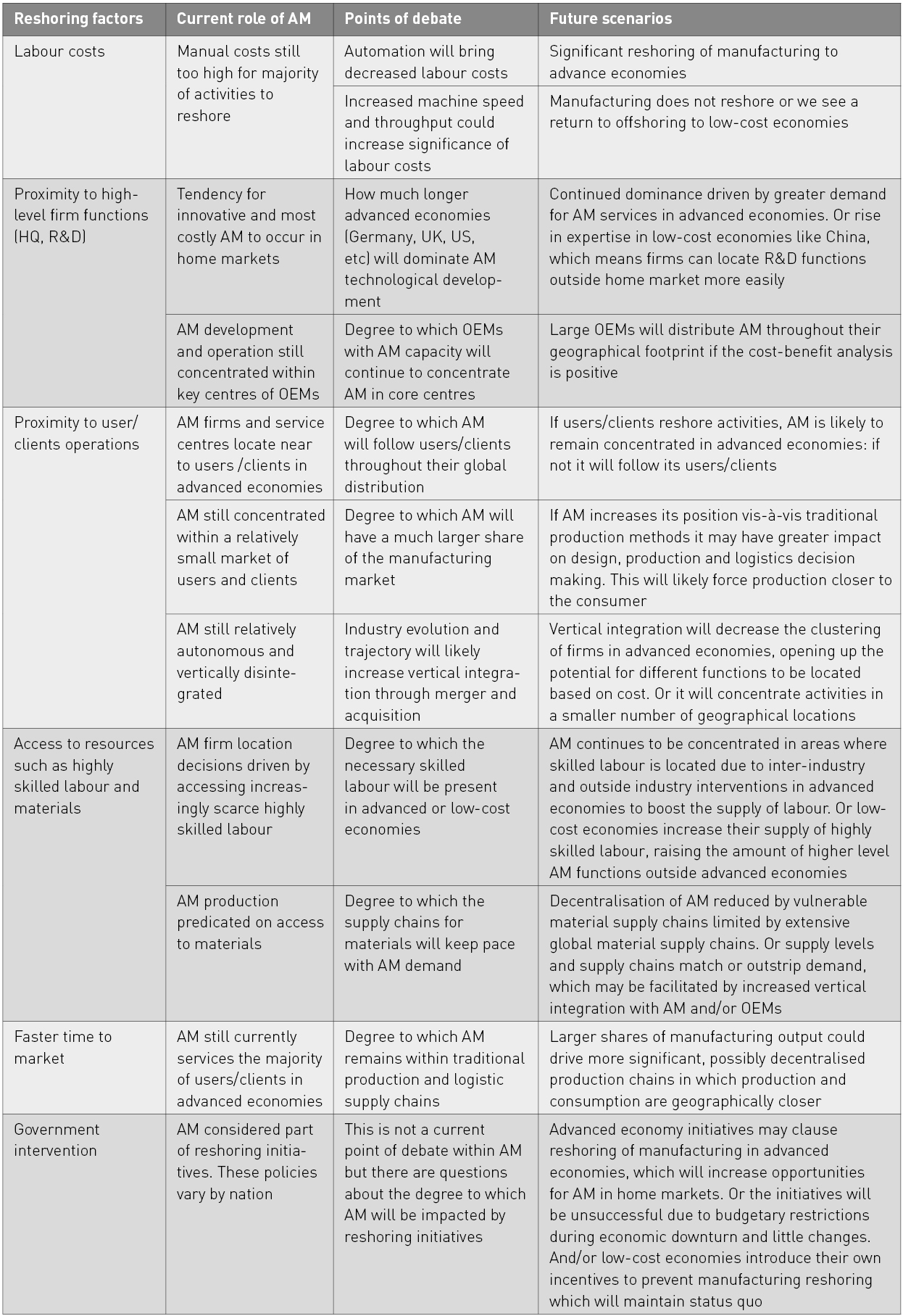

To summarise, there is currently scarce evidence that AM is impacting the geographies of production. There are anecdotal examples of some prototyping and injection moulding work returning from China, but at present, any reshoring that is occurring appears to be caused by broader shifts in the cost-base of manufacturing rather than by AM technologies. We are therefore in a period of anticipation in which there are several directions of change. Table 2 charts the key factors involved in reshoring, applying these to AM and outlining the possible future scenarios. The degree to which metal AM could transform existing geographies of production is dependent on machine speed and throughput, material supply and access to skilled labour, labour costs and the composition of the AM sector as a whole. In the short term, it appears likely that the status quo will remain. Longer-term, it is likely that existing production will remain dominated by traditional organisational geographies but that newer products that are designed for AM will be able to be produced closer to the consumer – be that in advanced or low-cost economies – using the (projected) expanded global networks of AM firms and OEMs.

As one interviewee sought to remind us: “Money controls everything and unless there is an economic financial reason to change something, it doesn’t change.” It is most likely that a global transformation in the location of manufacturing will be precipitated by larger global crises, such as peak oil and/or climate change significantly increasing the cost and vulnerability of long distance supply chains. Here we would see a shift to more regionalised or localised production, in which AM would play a significant role. We can therefore suggest that AM may not cause geographical changes, but it will likely play a crucial role in solving the problems that will emerge, with a particularly significant role for metal AM.

Metal AM, Industry 4.0 and the Factory of the Future

The metal AM industry is evolving rapidly. Some aspects of that change are clear and relatively uncontested, such as the diversification of applications from prototyping to functional parts. Others are more hotly debated, including where improvements need to be made (equipment, materials, supply chains, or all of these), where the greatest growth potential lies (sectoral and geographical) and how the industry should be most efficiently organised in the future. Given the huge pressure of expectation being exerted on AM – and metal AM in particular – by policymakers, this article will conclude with some reflections on how metal AM may be part of this almost universally adopted vision of our manufacturing future.

Surprisingly, some members of the community still felt that the notion of AM machines being integrated on the factory floor was in the distant future. “I’ve never seen it. The cost of the machines is a barrier to this,” stated one. Others felt that changes were already happening as part of the process of moving toward the Factory of the Future: “AM is a big part of the factory of the future. As new (products) are developed we see production changing – the production line for each generation of [our product] has changed. Robotics, automation will feature. AM is also used in supporting [our product] i.e. printer at maintenance site. We can send the design standard for printing on site.”

Overall, metal AM is preparing itself in numerous ways for the future, anticipating that several aspects of contemporary methods and processes will have to change. “We are rapidly heading towards AM’s role in the factory of the future with automation and robotics. I think the whole transformation of the digital factory, where we can go all the way from design to really looking at modelling and simulation to manufacture, to inspect, I really think the next frontier is going to be software,” stated another source. In terms of timescale, the automated factory of the future, understood as a lights-out factory containing AM machines combined with post-processing equipment, was estimated to be at least five to ten years away. This is later than policymakers are anticipating. For several interviewees, reflecting on their own corporate and industry-wide strategies emphasised the need for long-term continuous improvements to alloys, powder quality, powder management and management systems to ensure process stability and control.

At present, the metal AM industry is offering a compelling case for increased public and policy interest and support. It combines technological innovation and is evolving quickly to develop the systems and standards that are needed to appeal to a wider user-base. Benefits may be gained from interaction with the ‘other kind of scientist’ (social scientists), who can offer a broader perspective on the industry; how it is changing, competing and helping to redress the imbalance created by all the hype around Additive Manufacturing.

Author

Dr Jennifer Johns

Reader in International Business

Department of Management

University of Bristol

Howard House

Queen’s Avenue

Bristol

BS8 1SD

The author acknowledges the contribution of the British Academy (award number SG162550) and the contributions of the research participants.

LAST MONTH’S MOST-READ ARTICLES