Additive Manufacturing Strategies 2026: Strategy without the strategy-speak in a maturing AM industry

Additive Manufacturing Strategies 2026 offered a revealing snapshot of an industry entering a more sober phase. The discussions in New York were less about disruption and more about execution: how capital cycles shape machine sales, why software and ecosystems may determine who scales, and where polymer and metal Additive Manufacturing follow very different economic paths. If there was a common thread, it was that AM’s future will depend less on technology claims and more on solving specific industrial problems. Joseph Kowen reports. [First published in Metal AM Vol. 12 No. 1, Spring 2026 | 15 minute read | View on Issuu | Download PDF]

If the name Additive Manufacturing Strategies suggests some clean, business school-case-study exercise in which a wise industry ascends a mountain, receives a tablet of principles, and returns with the AM strategy, AMS 2026 did its best to slay that notion. That is probably a good thing.

One implied lesson from the breadth and range of presentations at this year’s New York gathering was that ‘strategy’ in AM is not a singular term. It is contextual, sector-specific, and often technology-specific. It may mean consolidation for one company, workflow discipline for another, overcoming qualification challenges for a third, and simply surviving and growing for a fourth. It can mean one thing in desktop polymers, another in advanced aerospace polymers, and something else entirely in metal AM, where price structures, qualification burdens, machine costs, and application economics are meaningfully different.

That distinction matters for Metal AM magazine readers. AMS is not a metal-only conference, nor was this year’s edition framed that way by the organisers. It was a broad AM leadership event, with speakers from across polymer and metal, and presenters from a wide range of verticals, including dental, medtech, rail, aerospace, and defence. The conference is positioned as an “industry touchstone” that covers the topics most critical to Additive Manufacturing as a whole, not just one material class.

Still, some of the most useful ideas presented in New York do translate directly into the metal world. Others do not. And this, more than any slogan about “strategy,” was one of the most useful takeaways of the conference: polymer and metal AM are not merely variants of the same business model with different powders or feedstocks. They are usually different economic animals.

That is why it is worth being careful with generalisations. A lesson from Formlabs, Carbon, or Stratasys may be valid in their own context and still require translation or clarification before it applies to metal. In polymers, especially at the lower end of the market, price convergence with conventional manufacturing is more easily observed. Machine prices are lower, throughput can be higher, and in many cases, parts are good enough and at the right price. In metal, by contrast, the premium of AM over conventional production remains significant. That means the break-even quantity is lower in some cases, meaning that the economic justification usually has to be stronger on other grounds: lightweighting, part consolidation, inventory reduction, thermal performance, or some combination of the above. Metal AM still has to explain itself more often and more rigorously than polymer AM does.

So perhaps the right way to think about “strategies” at AMS is not as doctrine, but as precedent: examples, learned behaviour, business patterns, warning signs, and success stories. Not a promised AM land, but a set of maps – some drawn up for the polymer world, some for metal, and a few drawn at a high enough altitude to be relevant to both.

Blizzard as conference curator

There was, of course, another force shaping AMS 2026: the weather. The conference opened in the wake of a severe Northeast blizzard that forced travel cancellations and brought New York City its first blizzard warning in nine years. Central Park recorded 50 cm of snow, while parts of the broader region saw well over 76 cm; Rhode Island’s T.F. Green Airport registered 96 cm over two days, an all-time local record.

One is tempted to conclude that the organisers planned it this way all along: summon a historic storm, filter for only the hardened, the proximate, the stubborn, and the talented at rerouting air itineraries and even – horrors – using East Coast trains (including your diligent correspondent), and then let camaraderie do the rest.

Jokes aside, the weather gave day one an unusual atmosphere. Attendance was visibly lighter than normal, but the people who made it in were there to talk. The result was a lower-stress, more direct, more universal tone than one often gets at a packed event. According to post-event coverage, the conference retained its energy despite the disruption, and the organisers worked quickly to reconfigure schedules and cover for missing presentations. The substance of the event, in the end, did not appear to suffer significantly.

One might argue that AMS accidentally rediscovered something conferences often forget: when the crowds thin out, people tend to speak more openly. With fewer distractions and less pressure to rush between sessions, conversations become more direct. Not that we can expect the organisers to willingly repeat the apparent success or a more laid-back atmosphere anytime soon!

The keynote thread: AM is maturing, not failing

The most consistent message from the event’s senior voices was not chest-beating about great achievements, about which there are many anecdotes rightfully worth telling. It was something more sober and more useful: Additive Manufacturing is maturing, and maturity does not always express itself in a simple growth curve.

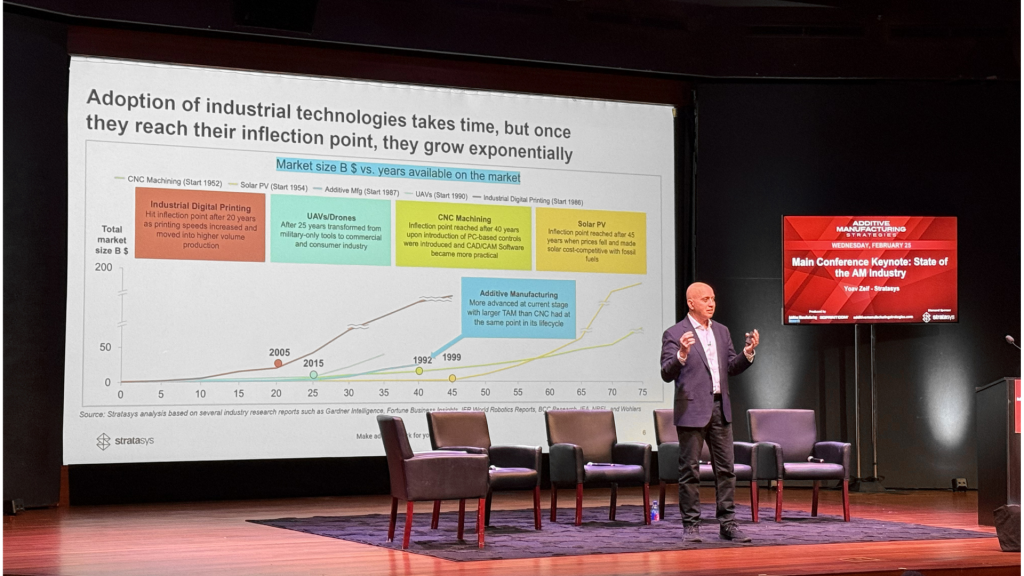

Yoav Zeif of Stratasys framed this particularly well. He argued that the industry’s recent struggles should not be mistaken for a crisis. Industrial AM machine sales have been hit by macroeconomic headwinds and a challenging financing environment, but capital-equipment industries are cyclical by nature. Companies buy machines, then take time to qualify them, integrate them, ramp them, and seek return on investment before buying again. That is not uniquely an AM problem; it is a capital goods problem. Zeif’s more provocative point was that the additive industry has perhaps spent too long talking as if faster growth were owed to it by historical destiny. AM is not exempt from the long slog that other manufacturing technologies have faced. Case in point: the CNC industry took a long time to mature and become mainstream. If that is a yardstick, then AM need not be ashamed of its growth trajectory, even though it is routinely castigated for slower-than-desired growth.

That line of thought was echoed by Brent Stucker, drawing on fresh Wohlers Report data. The headline numbers – roughly a $24 billion industry, still growing, with services remaining especially important – were, in his view, less striking than the idea that additive creates enormous value. Still, much of that value is captured downstream by end users rather than by the machine, software, or materials suppliers themselves. That is particularly relevant to metal AM, where the strategic question is often not ‘how many machines can be sold?’ but ‘who captures the economic value from the performance improvement or supply-chain advantage?’

Arno Held of AM Ventures also addressed the point. His thesis was that the industry has suffered not from a lack of capital, but from too much poorly allocated capital chasing too many versions of the same story. He argued that AM has too often behaved like a Swiss Army knife – many things done reasonably well, too few done exceptionally. The winners, in his formulation, will not be the companies that begin with a technology and then go searching for a problem. They will be the ones who know an application deeply enough that AM becomes the enabling method rather than the headline.

This matters for metal. Metal AM has often justified itself precisely through indispensability: better heat exchangers, turbine performance, geometries impossible or uneconomic to produce by machining or casting, supply-chain resilience, repair, and critical spares. In other words, metal AM has always had to live closer to Held’s world than some of the polymer market has. It may be one of metal AM’s strengths.

Polymers and metal diverge

Max Lobovsky of Formlabs, Phil DeSimone of Carbon, Yoav Zeif of Stratasys, and Brigitte de Vet-Veithen of Materialise all offered the same conclusion: the industry took too long to focus on customer outcomes rather than on technology descriptions.

For the polymer-oriented businesses, one recurring theme was the astonishing speed with which low-cost, easy-to-use systems have changed the market. Lobovsky was admirably blunt about this, openly pointing to Bambu as a serious industrial fact rather than a hobbyist footnote. Whether one agrees with all his comparisons, the strategic lesson is unmistakable: affordability, usability, and robust, user-friendly software can change a market faster than incumbents expect. Lobovsky went so far as to express regret that he had not moved faster in the early days of Formlabs.

For Metal AM readers, however, this lesson is only partly applicable. Metal AM cannot simply replay the desktop polymer script at higher prices. A more affordable metal machine is welcome, and we have recently seen movement in the low-cost metal systems space. A simpler user experience is also welcome, and so is better software. But none of these, by themselves, erase the deeper cost and qualification structure of metal production. Metal AM is more often slowed by certification, yield consistency, powder economics, post-processing, quality assurance, and the need to make a much stronger case for each application. The most important lesson from several CEOs is therefore not to follow the polymer path. It is better to focus relentlessly on where ease of use, workflow simplification, and cost reduction genuinely unlock demand.

Glynn Fletcher of EOS made an especially important point in this regard: the real competition is not other AM firms. It is conventional manufacturing. AM companies still too often talk as though their main strategic challenge is winning share within a niche sector, when the larger question is how to take work from machining, casting, moulding, and inventory-heavy supply chains. Metal AM is particularly exposed to this truth, because its most compelling results usually come when a metal part is not just additively made, but better justified additively than conventionally.

The software and ecosystem case

If one theme rose above nearly all others, it was the role of software and ecosystems.

De Vet-Veithen provided perhaps the conference’s clearest analogy, comparing AM’s current state to pre-container shipping. Before standardised containers, transport worked, but badly: fragmented handoffs, incompatible infrastructure, poor visibility, lost goods, and needless inefficiency. Containerization did not just make ports more efficient. It transformed global logistics and enabled new business systems.

She argued that AM today still resembles that pre-container world: too many disconnected tools, too many incompatible workflows, too much local optimisation, and not enough system integration. Hardware innovation remains essential, but hardware alone will not scale the industry. AM needs a common language, software interoperability, and true workflow integration – what she and Karsten Heuser of Siemens Digital Industries both described in different ways as the basis for scaling the industry.

Heuser’s presentation extended the argument from software into manufacturing systems. For him, additive is just one layer in a larger next-generation manufacturing environment: automation, industrial AI, digital engineering, and full workflow integration. His examples ranged from rail spares to furniture to aerospace components, but the deeper point was that additive’s next phase depends on achieving better industrial execution. Additive should be a single integrated option across design, simulation, qualification, and production.

This is a particularly powerful point for metal AM. Metal’s biggest commercial successes rarely happen because customers want a metal AM machine. They happen because a customer wants a better thermal solution, a lighter aerospace bracket, a spare part delivered without tooling, a medical implant customised in days, or a repair pathway that saves inventory and downtime. In all of those cases, software and workflow are not back-office conveniences. They are part of the value proposition.

Another perspective on the software backbone required for distributed manufacturing came from Lior Polak of Assembrix. His presentation focused on trust in digital manufacturing networks. If Additive Manufacturing is to move toward geographically distributed production – additively manufacturing parts close to where they are needed rather than where they were originally designed – then protecting intellectual property becomes a central issue. The company’s approach can be particularly relevant for metal AM, where part value and IP sensitivity are often high, and where sectors such as aerospace, defence, and oil & gas increasingly view distributed manufacturing as a means of strengthening supply-chain resilience. In such environments, secure software infrastructure is not merely a technical convenience; it becomes a prerequisite for scaling AM across multiple locations.

The announcement at AMS that the Leading Minds and AM I Navigator initiatives would join forces was fitting in this context. The symbolism matters: an industry that still competes fiercely can nevertheless benefit from shared, non-proprietary discussion around terminology and adoption. There are few opportunities for senior leadership to meet outside the commercial pressures of a trade show; when such a forum produces even modest cooperation on common problems, that should be viewed as progress.

Metal AM themes

For all the broad AM themes, AMS 2026 did offer plenty of metal-specific material. Heuser’s emphasis on aerospace, rail, and industrial integration was important, in part, because these are sectors where metal AM’s logic is stronger than average.

Stefanie Brickwede of Deutsche Bahn provided a particularly concrete illustration of how this logic plays out in practice. Deutsche Bahn has spent years building one of the most extensive AM spare-parts programmes in the rail sector, qualifying built components for use across a fleet that spans multiple generations of rolling stock. The challenge is not simply to additively manufacture a part once, but to establish the certification, documentation, and digital traceability required for repeatable use in an operational rail network. Brickwede emphasised that AM allows operators to address the long-tail problem of spare parts for ageing equipment, where tooling has disappeared, and conventional supply chains have little incentive to reproduce low-volume components.

Tom Nogueira and Bryan Wisk, speaking around the Desktop Metal – Arc Impact structure, made the case for Binder Jetting (BJT), not as a generic industry-saving story but as a platform that may be especially compelling in metals and ceramics where materials, microstructure, and supply-chain needs align. Their focus is on nickel superalloys and silicon carbide. Broader advanced materials work underscored an important truth: metal AM’s future may rely less on winning the same familiar applications more cheaply and more on proving out materials-and-process combinations that conventional workflows struggle to supply.

Many of the opinions expressed reinforce the same conclusion for metal AM: strategy is not an abstract exercise. It is the hard work of deciding where metal AM solves an expensive, painful, recurring problem better than any alternative.

That is why the defence and aerospace theme, raised by multiple speakers, deserves particular attention. Zeif pointed to aerospace and defence as among the most exciting near-term opportunities. Heuser tied additive to rail, aerospace, and industrial AI. Panel discussions on venture funding repeatedly returned to defence and distributed manufacturing. In metal AM, these sectors matter not just because budgets are large, but also because they value what metal AM is comparatively good at: high-value parts, low-to-medium volumes, complex logistics, and the premium placed on speed.

In polymers, affordability may be the dominant factor. In metals, urgency, mission value, and performance often matter just as much.

The more counterintuitive lessons

The industry’s problem may not be too little demand, but too much fragmentation

De Vet-Veithen, Heuser, and Held all reached this conclusion from different angles. The issue is not that AM lacks basic use cases. It is that too much of the workflow remains disjointed and expensive, and too many companies still speak in process terms instead of customer terms.

Low-cost systems are not just a hobbyist story

Lobovsky’s remarks about Bambu, however uncomfortable for the industry in Western countries, were important. This does not mean that desktop Additive Manufacturing economics translate neatly into metal. It does mean that industrial players should not treat cost reduction and usability improvements as peripheral to ‘serious’ AM.

AM adoption remains slow – perhaps because the industry has yet to adopt a manufacturing mindset

Zeif was particularly clear on this point. It is striking that even basic metrics such as Overall Equipment Effectiveness (OEE) required years of discussion among sophisticated industrial participants. That is not a sign of failure, but rather that AM is still learning to behave more like mature manufacturing.

AI is useful – but not magical

Here again, there was convergence across speakers. Lobovsky, Zeif, DeSimone, de Vet-Veithen, and Fletcher all treated AI as a genuine lever for speed, design assistance, service, and internal efficiency. But de Vet-Veithen’s caution against another hype cycle was well taken. The most credible AI examples at AMS were not grand proclamations; they were concrete improvements: faster medical workflows, better service tools, smarter coding, tighter build accuracy, and the possibility of better designs sooner.

China is no longer a concern for the future. It is a present competitive fact

De Vet-Veithen said outright that the industry took too long to take Chinese competition seriously. That point also surfaced during market analysis sessions. For metal AM, this is not only about machine pricing. It is about supply chains, clusters, domestic competition, and the ability to scale around ecosystems rather than around isolated companies.

Repeat orders matter more than heroic first sales

This point came through especially clearly in the market intelligence panel. A first machine sale is good. Repeat machine sales and material orders are better. In metal AM, where application development can be long and engineering-intensive, repeatability is the real strategic signal that something is working.

What AMS is for

Fig. 8 Panel discussion ‘Perception is Reality: The Public Markets Narrative’ at AMS 2026 featuring Debbie Holton, Stephan Bulkow, and Aaron Muller (Courtesy Additive Manufacturing Strategies)

There remains a strong case for an event like AMS. The industry does need a forum that is not simply a trade show floor adorned by a conference. There is real value in getting senior management, researchers, investors, software people, OEMs, and users into the same room without the full commercial velocity of a normal exhibition. The event’s relative intimacy – helped this year, ironically, by the storm – encourages a more candid exchange.

The discussions in New York also underlined how broad the idea of “strategy” in Additive Manufacturing has become. Depending on the company and the sector, strategy can mean industrial integration, software ecosystems, supply-chain resilience, application development, or simply learning how to scale adoption under more difficult economic conditions. That breadth was itself revealing. The industry is still working through what strategy means in practice.

The distinction between polymer and metal Additive Manufacturing remains important in that context. Some themes clearly cut across both domains, while others reflect very different economic and operational realities. The discussions that acknowledged those differences often yielded the most useful insights for attendees trying to translate broader AM themes into their own industrial context.

AMS 2026 did what a mature industry conference ought to do: it encouraged participants to think beyond hype, beyond technology labels, and beyond easy narratives. What emerged was an industry trying, imperfectly but seriously, to grow up. For Additive Manufacturing, that may be strategy enough for now.

Author

Joseph Kowen

Joseph is an industry analyst and consultant who has been involved in AM since 1999. He is an Associate Consultant at Wohlers Associates, part of ASTM International’s AM Center of Excellence.

www.linkedin.com/in/joseph-kowen-a5129b3/

AMS 2027

AMS 2027 takes place from February 23–25, once again in New York City.

LAST MONTH’S MOST-READ ARTICLES