Predicting the metal Additive Manufacturing market – and breaking the hype cycle

Additive Manufacturing has experienced significant growth over the past thirty years. However, many market players have found themselves disappointed with current market volumes compared to earlier projections for the industry. Today, the AM industry is at an intriguing stage. Depending on your perspective, it can appear to be either declining or thriving. How do these perspectives align, and how is its current status represented by data and forecasts? AMPOWER's Maximilian Munsch, Eric Wycisk and Matthias Schmidt-Lehr share their assessment and consider the challenges of predicting a highly-complex industry. [First published in Metal AM Vol. 10 No. 2, Summer 2024 | 15 minute read | View on Issuu | Download PDF

With the introduction of direct metal Additive Manufacturing machines and the expiration of early patents in polymer AM ten to fifteen years ago, Additive Manufacturing was expected to become a game-changer for serial manufacturing. Driven by the hype, specialists and large management consultancies alike predicted a prosperous future market with significant profit opportunities for every major company. This anticipation led to substantial investments from global corporations and heavy funding into numerous startups.

While the industry has indeed grown substantially over the decades, there are signs that the market could be reaching its first saturation point, with a multitude of companies offering a variety of technologies, platforms, materials, services, and software solutions. Today, only around 2,000 metal AM machines from twenty different technology derivatives are sold annually by nearly 200 machine OEMs. This ratio resembles more of a specialised machinery market than a fast, scalable machine business model, which may explain some of the frustration among current market players.

Still, all major AM reporting organisations agree that metal AM will continue to grow and achieve a double-digit growth trajectory over the next five years, and user feedback from major industry players supports this claim of increased adoption – but this is where the consensus among reporting publishers often ends. A closer look at the market numbers reveals significant differences in both current figures and five-year projections. This article dives deeper into how AMPOWER Report data are generated and the challenges that must be overcome. It begins by examining the current market conditions and trends in the metal AM industry as outlined in the report.

Overview total metal AM market

The past year presented considerable challenges for the metal Additive Manufacturing industry, marked by intensified competition among equipment suppliers and a steady influx of new market entrants. A general market slowdown in 2023 in terms of unit sales combined with market saturation among suppliers, difficulties in product differentiation, and concerns over profitability have led to low stock market valuations and sparked discussions of consolidation.

In particular, suppliers from the Asian market are increasingly aiming to expand their presence beyond domestic borders to attract customers. Established players are closely monitoring Chinese Powder Bed Fusion (PBF) suppliers, who are rapidly expanding their product portfolios. These suppliers are introducing machines with increasingly large platforms and dozens of lasers at competitive price points.

In recent months, public metal AM companies like Desktop Metal and Velo3D have experienced low stock valuations, reflecting investor hesitation likely stemming from ongoing profitability concerns. This trend underscores the broader challenges faced by the industry, including global economic uncertainties and high capital costs. It also reveals that the market was overhyped and overvalued for many years; investors and C-level decision-makers were drawn to the repeatedly touted message that metal AM is a technology ‘no one can afford to miss.’ But funding and valuations were based on market multiples that projected unreasonably high results and ignored rational factors. These multiples have now crashed to below 1 for value over the next twelve months’ revenues. Consequently, the claims made by Additive Manufacturing industry founders are now being scrutinised more closely, as many once highly valued startups still lack the promised profitability years later.

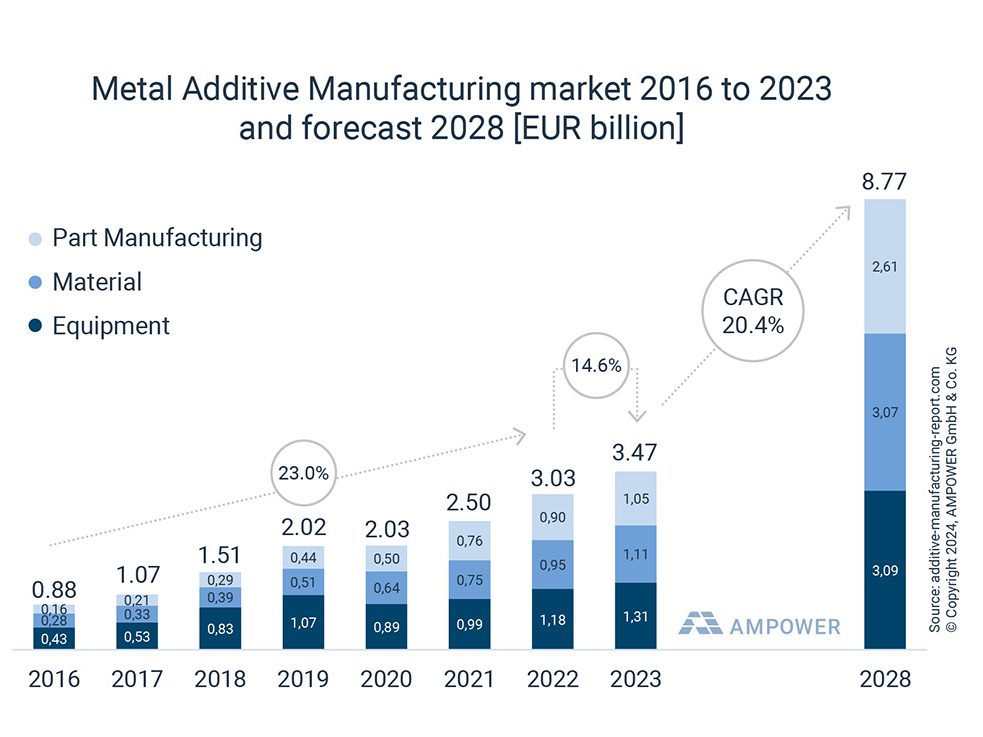

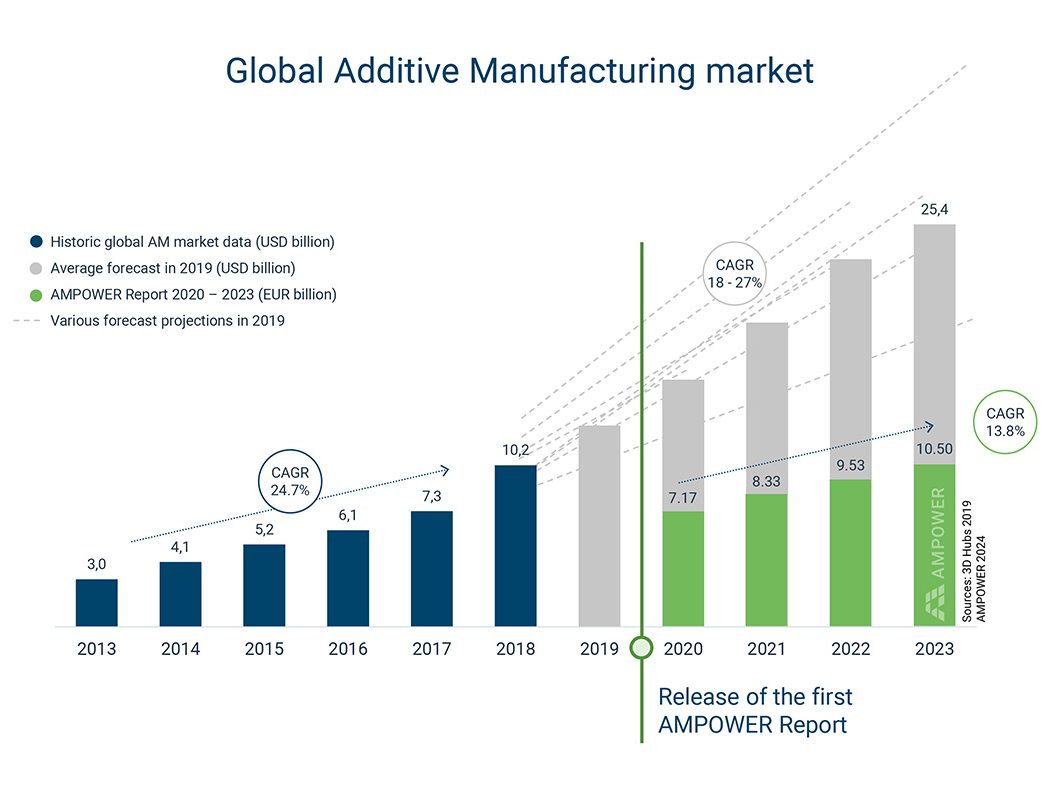

Despite these difficulties, the metal Additive Manufacturing industry achieved a double-digit growth rate of about 15% in 2023, outperforming traditional manufacturing sectors and demonstrating resilience in challenging conditions. Looking ahead, both buyers and suppliers in the Additive Manufacturing industry maintain an optimistic outlook, anticipating an annual growth rate of around 20% (Fig. 1). They foresee substantial growth in the coming years and continued adoption across an increasing number of industrially significant applications in addition to those where it is already highly successful. Amid geopolitical tensions, for instance, there is potential for Additive Manufacturing to benefit from increased defence spending, as well as from growing demand for complex solutions and resilient manufacturing capabilities in other sectors.

General metal AM market trends

Search for profitability

As growth slows and profitability remains uncertain, industry consolidation becomes more likely. The product portfolios of various Powder Bed Fusion OEMs, for instance, are near identical, making it difficult to find their respective niche wherein they provide a unique selling proposition to users. Consolidating them into a single portfolio, however, holds the promise of blending the best features from many worlds.

This mass consolidation could also lead to synergy effects, particularly in cost savings for sales and marketing, which is currently estimated at around 20-30% of the revenue due to the complexity of their products; in contrast, other manufacturing industries like CNC typically have sales and marketing expense ratios ranging between 5-15%. Furthermore, there’s potential for additional cost savings through synergies in R&D, as PBF companies often follow identical or similar tracks in their development efforts to meet customer demands.

No more experimenting

The way end users have adopted metal Additive Manufacturing technology has evolved significantly over the past decades. In the 2000s, pioneers acquired machines primarily to conduct baseline studies and R&D work to explore the technology’s potential. The 2010s saw a surge in metal AM machine installations driven by curiosity and the fear of missing out on the next big innovation, with many aiming to jump directly into serial production.

A common misconception during this period was that Powder Bed Fusion would directly replace CNC machining on a wide range of products. In reality, however, PBF components often require lengthy redesign cycles, including rethinking and redesigning entire components and assemblies to harness the technologies’ benefits. Today, experimentation has mostly given way to strategic investment by industries with viable business cases in specific applications. Machines are purchased based on rigorously calculated business cases that must demonstrate economic feasibility. The introduction of metal Additive Manufacturing into various regulated environments has furthered the shift to serial production. A shared understanding within the industry regarding standardisation and qualification has helped reduce uncertainty and increase adoption, with regulatory and certification authorities supporting this shift by taking a more active role.

Applications are no longer visible to public; development in secret

Contrary to the early years, with continuous coverage of perceived breakthroughs and innovation leaps, a lot of today’s metal AM successes remain hidden from the public eye. Metal AM often serves as a key enabler for high-performance components that have significant impact on much larger products. Hence, IP concerns are often a reason for secrecy of the most attractive parts. For instance, Space X is reputed to have a significant PBF capacity and utilises AM extensively for new and efficient rocket components. However, the company has maintained a low profile regarding this technology in its press releases since 2017, aligning with its reputation for discretion.

Another example involves implant manufacturers who have been successful and highly profitable for over a decade in providing bone replacement parts made from titanium and cobalt chrome alloys. In their product advertisements, however, AM as a production technology does not play a major role, with the focus instead on the benefits of the product. This approach is fitting for a mature industry, where the emphasis shifts from the production technology itself to emphasising the additional value of the product.

Challenges in making AM market reports

The aim of a market report is to offer comprehensive and reliable insights and analysis of the current state, market trends, and opportunities to facilitate informed business decisions. These reports typically concentrate on specific areas (e.g. the metal AM industry) by evaluating factors like revenues, the flow of goods, and/or purchase criteria to derive requirements and actions for stakeholders. The approach to gathering this information varies depending on the specifics of the industry in question. However, creating a market report entails various challenges across multiple facets.

Model

The market model is crucial for accurately reflecting the condition of the market with the available dataset. It becomes particularly important when the analysis extends beyond simple summations of, for example, revenues, and requires imputations of missing data or scaling available data to the full size of the market. Such models are highly specific to a market. At AMPOWER, for example, the models differ between metal and polymer technology, as each has its own intrinsic specialities.

An important consideration when creating the market model is to initially define its boundaries. Metal AM, for instance, can be categorised as a niche industry within the manufacturing sector that is predominantly a B2B market. Its players – both on the supplier and buyer sides – are primarily active in countries with high-value production. Unambiguous is the inclusion of machine and material suppliers. Other entities that could be potentially included in such a model are providers of other related services and goods such as manufacturing services, peripheral equipment, software solutions or value of additively manufactured end user components.

A specific example in the metal AM market where reports often struggle to provide a clear answer is whether the value of the production output is added to the market size. At AMPOWER, we treat the goods and services from part manufacturing services as part of the metal AM industry, whereas AM products manufactured by the OEM (for instance a hip cup produced by an implant or contract manufacturer) is categorised as a good that is generating value within the medical industry, but not the AM industry. A similar discussion arises when considering the software market, where pure-play software products are limited and there is often a mixed use of software products such as CAD or MES functions for AM as well as other operations in a company.

Data acquisition

Typical approaches for primary data acquisition are standardised questionnaires, survey interviews, or analysis of secondary public sources. Questionnaires are essential to collect quantitative data such as revenues or installed machine base. Additional qualitative research is necessary to understand the context of the quantitative data and get a grasp of the trends. Public sources such as financial reports or economic databases provide additional insights and data points to round the model input.

It is, of course, challenging to gain access to this dataset. Of high importance are the sources for the data acquisition for the questionnaires and surveys. A large majority of the metal AM market suppliers do not publicly share financial data, recent developments or their long-term forecasts.

Segmentation

Other challenges come into focus when deciding on how to display the analysis results. Market research can easily yield thousands or more data points across various categories such as technologies, industries, regions and materials. The challenge here is then packaging this information into the correct segmentation that addresses the reader’s needs. For example, many high-level reports describe the Additive Manufacturing market with just one value for its total size, blending polymer, metal, and other material systems into one. The question arises: who is interested in this aggregated market, and what decisions regarding business strategy can be derived from it?

Analysts on the report’s customer side prefer data they can use in their specific business setting, neglecting all other input; a company working in metal AM is hence less interested in comparing their business success to developments from polymer AM. This allows them to assess the development of a market share for a technology or within a region and to eventually derive specific actions.

In a highly dynamic environment, these segmentations are not necessarily static as new customer industries or new technologies evolve or disappear quickly. This can prove to be a balancing act between providing consistency in data preparation versus the adaption to changing market conditions. Returning customers expect a recurring format as they would like to plug the report data into their internal templates to prepare the familiar analysis result.

One solution here could be to share the raw data, but this is not always a feasible alternative, as a lot of surveyed data is sensitive and confidential. Hence, segmentations have to be well-considered.

Forecasts

Forecasts play a major role in a market report as readers expect guidance on aligning their strategic direction. However, forecasting is a challenging topic as it attempts to provide a glimpse into the crystal ball. In the case of metal AM, a niche industry in a B2B environment, the straightforward approach is to analyse the expected development of the most important players that will likely dictate the market.

However, metal AM is a highly dynamic environment with numerous new entrants every year, many depicting fast growth with their solutions ‘tapping into the trillion-dollar manufacturing market’, as often exaggeratedly claimed, and solving its issues. These startups often aim to present an attractive value proposition to investors, depicting a very favourable but ultimately unlikely scenario.

New metal AM startups often lack true understanding of their value, leading to overly optimistic forecasts or overly conservative estimates that fail to capture the market’s true potential. The lack of experience-based projections can double the difficulty, as they may rely heavily on anecdotal evidence or incomplete market understanding. Consequently, accurately capturing market potential requires a delicate balance of research-based optimism and an understanding of the market’s evolving nature. Managing likely unreasonable exaggerations or lowballing projections is a challenge in such an environment.

When evaluating the historical data published in various reports, it becomes clear that the Additive Manufacturing industry has become a victim of a self-fulfilling prophecy. Inflated forecasts and expectations have led to a reciprocal buildup of growth expectations: the suppliers’ forecasts were based on the inflated expectations from the reports, which in turn led to high values in the reports. An assessment in hindsight of several market predictions and AMPOWER’s assessment to the total market size of polymer and metal AM is shown in Fig. 2.

The AMPOWER approach

AMPOWER believes its role in the market is to provide an accurate picture of the current situation without perpetuating the overly optimistic hype of the 2010s. The AMPOWER Report represents one of the latest reports in the AM market, allowing the team to design a market assessment methodology that aligns with the current market situation without being constrained by outdated models. The team identified two methodic differentiators aimed at adding more value and contributing to the accuracy of both the current market assessment and the forecast.

Confidentiality

When the first AMPOWER Report was generated, the industry was already significantly more competitive than in previous years. Anybody compiling market data was faced with challenges in acquiring highly sensitive sales data from non-public companies, which were not inclined to provide their business data due to slower growth than had been forecast. As a result, the AMPOWER team refrained from publishing any company-specific data and treats all shared insights discreetly.

Part of the AMPOWER methodology is to ensure complete confidentiality of all market numbers provided by companies. While this approach led to companies supporting the research by providing highly accurate numbers and a high response rate from market participants, it also had its drawbacks. Calculating market shares became more difficult for the readers of the report, and companies were unable to assess their competitors’ performance. Additionally, certain technology breakdowns or regional data was limited to prevent single-source providers in specific countries or technologies from being exposed in the detailed segmentation.

However, reflecting on discussions with report customers to refine the model and depiction of data, it became evident that specific company data is not necessary to describe market trends. Segmentation into technologies, for example, can provide sufficient insights into developments without highlighting specific market players.

User perspective

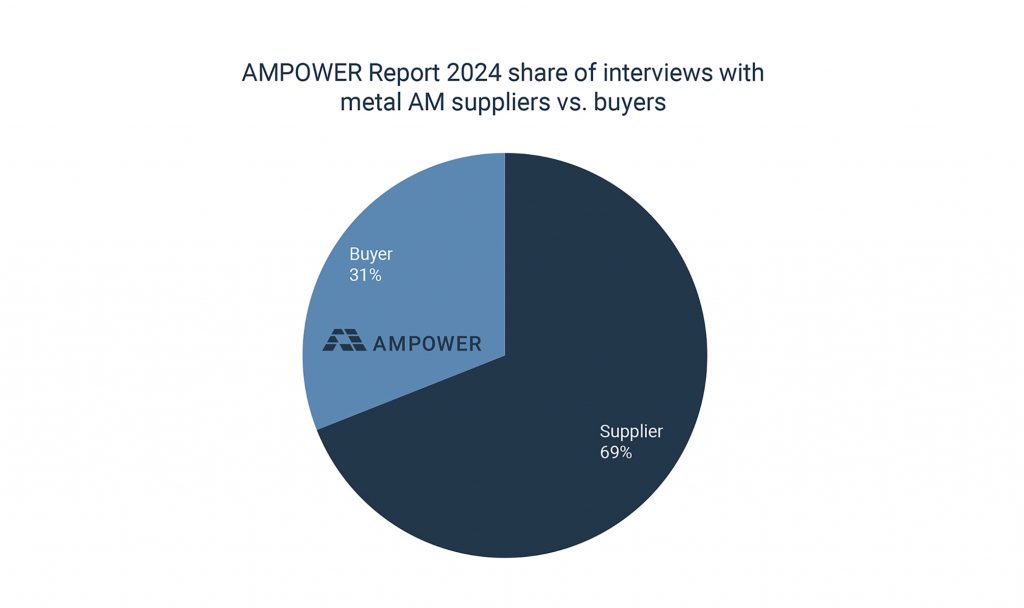

A view from metal AM users likely provides the most accurate market representation and forecast. In this more mature stage of metal AM, users can offer insights into future machine investments based on their current programme developments, adding bottom-up accuracy to the model. Additional datasets (e.g. current machine utilisation and material consumption based on user feedback) constitute the most accurate database on a global scale. While this methodology requires significant effort, it pays off in terms of data accuracy. In the recent survey for the AMPOWER Report 2024, 31% of the interviewees represented the buyer, or user, side, Fig. 3.

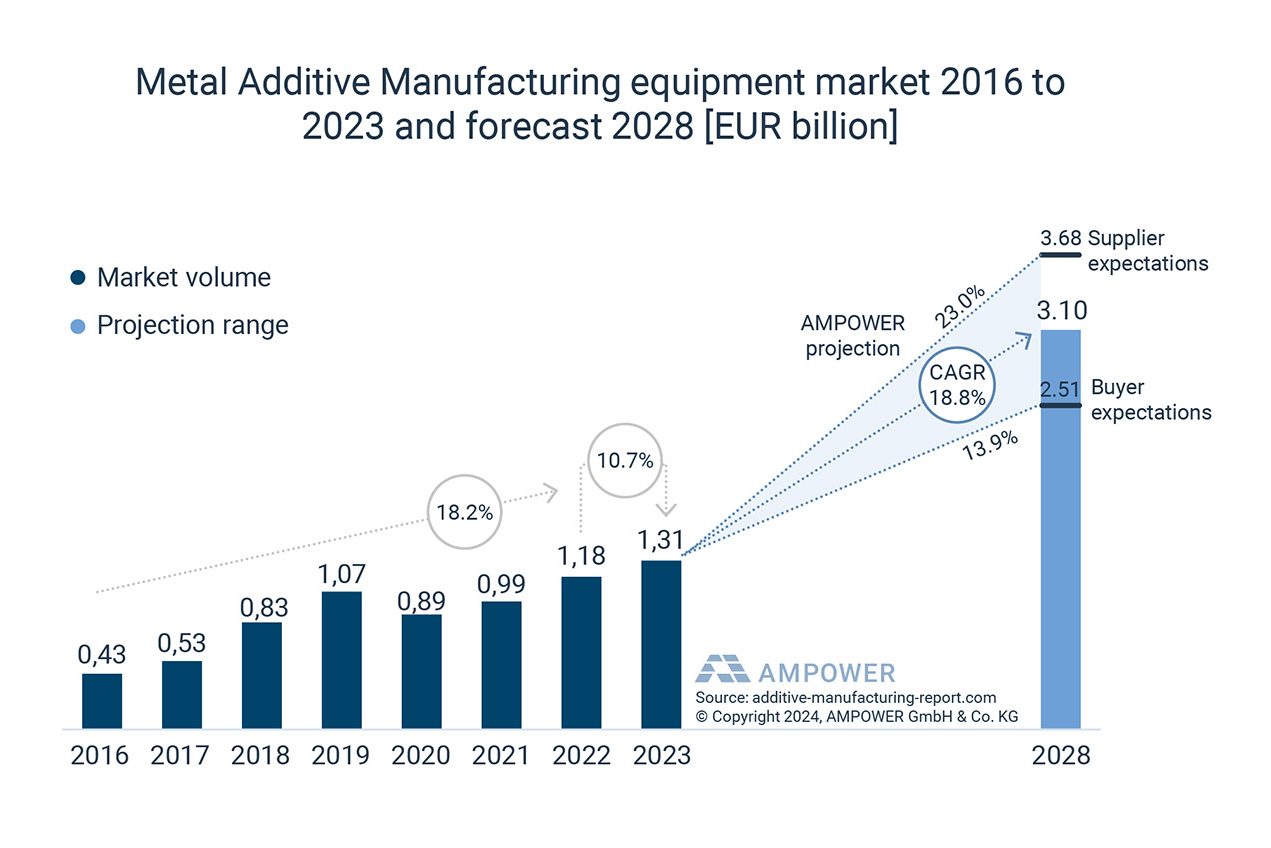

The user perspective is utilised in the AMPOWER Report to provide two different indicators for market forecasts. Over a five-year outlook, this buyer perspective allows for a reflection on supplier opinions. Users typically report lower market expectations compared to suppliers. For instance, projections of equipment revenue growth by suppliers stand at 23%, whereas users expect only 13.9% growth year-over-year until 2028, as shown in Fig. 4. Certainly, this data may reflect a bias towards known users today, but recent purchasers gain a higher weighting in the model to compensate.

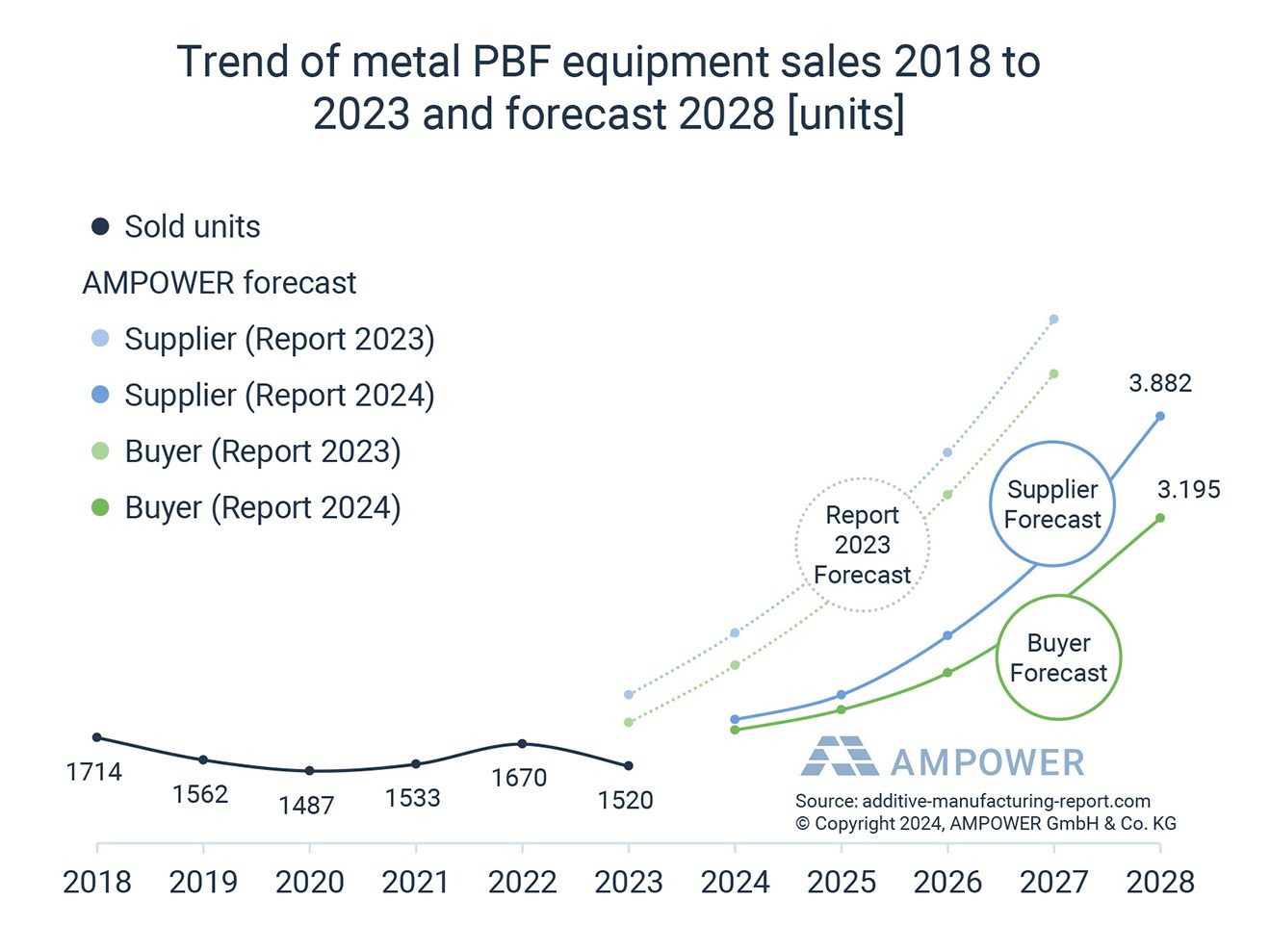

Established suppliers have adjusted their growth outlook over the past years, adopting the user perspective, which has proven to be closer to the actual value in hindsight evaluation, as illustrated in Fig. 5 on PBF equipment sales. This approach of taking into account additional factors rather than only questioning the supplier base led to a market valuation we have often heard from readers to be on the lower side compared to other reports; or, as we like to put it, on the realistic side.

Authors

Dr.-Ing. Maximilian Munsch

Dr.-Ing. Eric Wycisk

Matthias Schmidt-Lehr

AMPOWER

[email protected]

www.additive-manufacturing-report.com

LAST MONTH’S MOST-READ ARTICLES