AMS 2025 New York: A reality check for the Additive Manufacturing industry

AMS 2025, organised by 3Dprint.com and Additive Manufacturing Research, delivered a stark wake-up call for the Additive Manufacturing industry. Once hailed as a disruptive force, AM is struggling to meet high expectations, with large-scale industrial adoption progressing more slowly than anticipated. The event revealed a disconnect between bold financial projections and market realities, leading to a crisis of confidence among investors and stakeholders. Tali Rosman reports on an industry at a crossroads, facing hard truths and recalibrating for the future. [First published in Metal AM Vol. 11 No. 1, Spring 2025 | 15 minute read | View on Issuu | Download PDF]

The opening sessions at AMS 2025 set a stark tone, providing a long-overdue reality check for the AM industry. Yoav Zeif, CEO of Stratasys, addressed the industry’s struggle to meet the ambitious financial projections initially promised to investors. Despite being touted as a transformative technology, large-scale industrial adoption of AM has progressed slower than anticipated – a trend that has not gone unnoticed by financial markets.

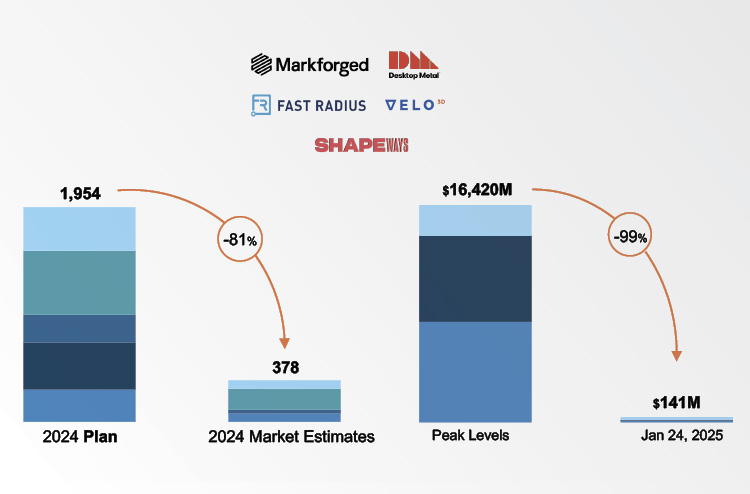

One of the most striking insights Zeif shared was precisely how vast the gap between expectations and reality is. SPAC-funded AM companies had projected nearly $2 billion in revenue for 2024. However, actual estimates now fall below $400 million – an 80% shortfall (Fig. 1). Even more alarming, the market capitalisation of these companies has plummeted from $16.42 billion to just $141 million – a staggering 99% decline. The numbers highlight a sobering truth: too many AM companies have overpromised and under-delivered, fuelling a crisis of confidence among investors and industry stakeholders.

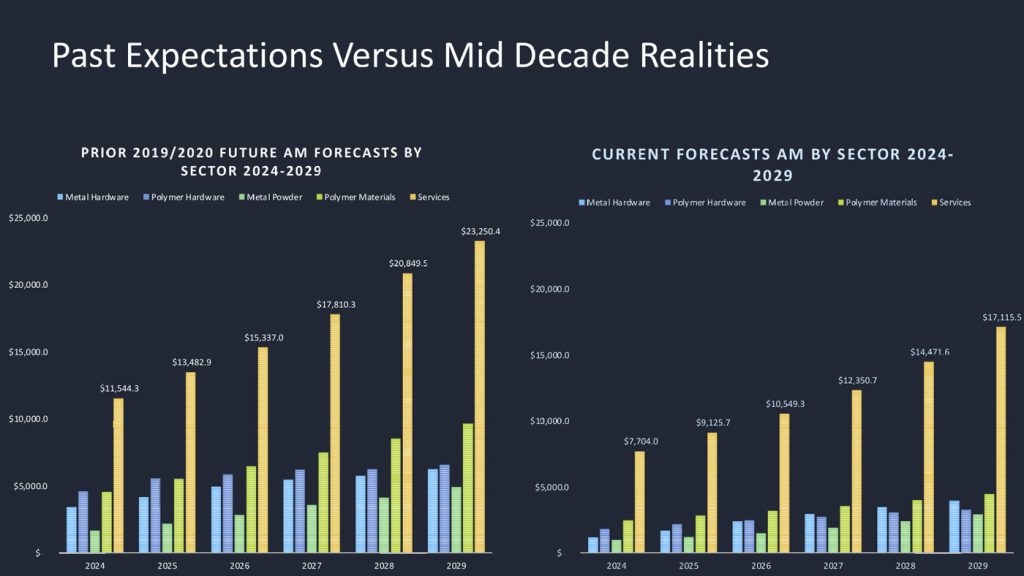

Following Zeif’s presentation, Scott Dunham, Additive Manufacturing Research (AMR), presented updated market forecasts, revealing further recalibrations in AM’s expected growth trajectory and lowering the industry’s CAGR (Fig. 2). This reflects a broader sentiment at AMS 2025, where it was clear that while AM still holds promise, it has not yet delivered the rapid disruption many had anticipated.

While all of this is true in the West, competition from Chinese AM companies is accelerating. Backed by aggressive government support and cost-competitive manufacturing, several Chinese firms have made significant strides – not only in the low-end market but also in high-end technologies such as Laser Beam Powder Bed Fusion (PBF-LB). This influx of lower-cost machines, bolstered by government subsidies and cost-competitive manufacturing, is making it harder for Western AM companies to compete.

The message to AM companies was clear: the industry needs to transition from disrupting to optimising manufacturing. BMW, the US Navy, and other major users echoed the same message: AM is not here to replace traditional manufacturing but to complement it. Brigitte de Vet-Veithen from Materialise captured this sentiment perfectly, urging AM firms to stop trying to win the Oscars for best performance and instead aim for best supporting role.

With these realities setting in, the industry stands at a pivotal juncture. If AM companies want to regain investor trust and drive broader industrial adoption, they will need to focus on proving reliability, improving cost-efficiency, and seamlessly integrating into established manufacturing workflows.

National security and AM’s strategic role

A central theme at AMS 2025 was AM’s role in national security, defence, and supply chain resilience. Matthew Sermon from the US Navy highlighted that while AM is making progress in defence applications, there is still a long way to go. The Navy has expanded its use of AM for submarine components, reporting that over 150 AM-produced parts are now in service, compared to fewer than ten just a year ago.

While AM is already playing a role in producing spare parts and reducing lead times, the DoD acknowledged that adoption at scale is still not occurring, citing bureaucratic hurdles, qualification challenges, and the slow-moving nature of defence procurement.

With that, Adele Ratcliff from the Department of Defense Office of Innovation Capability and Modernization highlighted that reshoring manufacturing is only a part of securing the supply chain. While there is a growing push to produce more parts using AM in the US, the materials supply chain remains a weak link. Many of the raw materials needed for AM – and for metal powders, in particular – are sourced internationally, with China controlling 90% of rare earth metals. Without a stronger domestic supply chain, AM’s potential to enhance national security will remain limited.

For AM to truly support national security, it is not enough to have Additive Manufacturing capability in key locations. Instead, the entire ecosystem, from material supply to post-processing, needs to be accounted for. Government initiatives in the US and Europe are working towards this goal, but there is still a gap between policy ambitions and industrial execution.

While AM’s role in defence is growing, it is worth noting the scale at which the commercial sector is adopting AM. For comparison, Deutsche Bahn has deployed 150,000 additively manufactured parts across 700 identified use cases, BMW mentioned 500,000+ series parts produced, and Airbus cited over 10,000 metal AM parts in use. While these figures are unrelated to national security and are not ‘apples to apples’ with the part numbers referred to by Sermon, they provide a helpful benchmark, demonstrating that while defence adoption is increasing, it still has a long way to go before it reaches this level of industrial-scale implementation.

Several promising initiatives were highlighted in this context. One is the upcoming launch of the Future Alloy Study & Testing (FAST) Center, a public-private partnership between Scot Forge and the Department of Defense. Designed to accelerate the development and qualification of advanced metal alloys for defence applications, the FAST Center will be capable of conducting thousands of tests within weeks, significantly reducing traditional timelines.

Another notable initiative is the Stifel North Atlantic AM-Forward Fund, recently launched to provide growth capital to small and mid-sized US manufacturers in the aerospace and defence sectors, with a focus on AM. Operating under the SBA-DoD SBIC Critical Technologies (SBICCT) initiative, the fund leverages private capital alongside SBA support to advance critical national security technologies. It offers structured debt financing with equity-linked instruments and received its SBIC licence in October 2024. Key investors include Lockheed Martin and GE Aerospace.

How AM machine OEMs can win: focus on value capture and integration

At AMS, industry leaders emphasised that AM machine OEMs in AM are most successful when they focus on value capture through applications rather than hardware sales. Panellists, investors, and industry leaders emphasised the importance of aligning revenue models with customer outcomes, integrating seamlessly into production workflows, and shifting from merely selling technology to delivering end-to-end solutions.

The ‘pure printer play’ is struggling financially, and panellists stressed that application-driven business models are more sustainable. Companies focusing on solutions – delivering high-margin, AM-enabled products – capture more value than those relying solely on machine sales. A prime example is LightForce Orthodontics, which uses AM to produce custom braces and is, in fact, a dental company, not an AM company. Other examples include Seurat and Fabric8Labs – both AM technology companies – who emphasised their application-first strategies, focusing on delivering high-value parts rather than selling printers.

Carbon offered a different ‘twist.’ The company’s CEO shared that the company’s salespeople are measured on customer usage and not on ‘box sales,’ directly connecting their compensation to customer success.

The conference also revisited a familiar but underutilised concept: Total Cost of Ownership (TCO). Several speakers stressed that evaluating AM through TCO rather than cost-per-part could expand the market’s potential tenfold. The value of AM lies beyond unit costs; it includes benefits such as faster time-to-market, improved performance, simpler logistics (e.g. due to part consolidation) and supply chain security. However, while TCO adoption is a goal, it remains aspirational rather than standard practice, with one panellist noting that “TCO thinking is still more discussed than implemented.”

Despite AM’s advantages, BMW reminded attendees that material costs remain a significant barrier to AM’s broader adoption in production environments, noting that without substantial reductions in material costs, AM will necessarily remain limited to prototyping and high-end applications. Further, BMW stressed that AM OEMs should stop thinking that they deserve special treatment.’ To be in production, AM OEMs must step up – not just in materials prices but also in machine reliability and uptime, in integrating into existing software tools, and in automation. In short, integrate instead of isolate.

This sentiment was also expressed in the ‘The Industrialization of Additive for Aerospace’ panel, where, in the context of PBF-LB, it was discussed that part consistency is unfortunately ‘not always the norm.’ It was noted that this is not an issue with machining, for example, yet it is commonplace with AM, and indeed this is a significant barrier to broader adoption. Briefly put, AM needs to be held to the same standards as other manufacturing technologies.

This means business model innovation is as crucial as technological innovation. Companies that build models aligning their success with customer outcomes – through application-first strategies, a focus on customer success, and integrated production workflows – will lead the next chapter of AM.

A final crucial point is the need for financial discipline. In recent years, many AM companies, supported by cheap capital, have overspent themselves into financial instability. Shapeways provides a stark example of this. The company went public in 2021 through a SPAC merger, resulting in a highly inflated valuation. However, it filed for bankruptcy in 2024, losing hundreds of millions of dollars, only to be bought out of bankruptcy shortly after. Marleen Vogelaar, CEO of ‘Shapeways 2.0,’ reflected on the excessive corporate spending and high ‘Wall Street’ salaries that characterised ‘Shapeways 1.0,’ noting that the new Shapeways is significantly more financially disciplined and profitable.

Investor sentiment: AM startups must pivot

AMS featured speakers from several investment firms, including AM Ventures, Bessemer Venture Partners, Eclipse, Exposition Ventures, AE Industrial, and North Atlantic Capital. On a positive note, the high attendance from investors in spite of the disappointing performance of past AM investments signifies there is still faith among investors in the potential of AM. However, investors now demand more structured, value-driven business models. A key message was the need to position AM companies as product-focused businesses rather than just technology providers. Several AM companies have echoed this investor investment, from Stratasys’ Lego blocks example – customers want the ‘assembled Lego blocks’ (i.e. the product, and not the individual blocks to put together themselves) – to the previously mentioned examples of Seurat and Fabric8 Labs.

Scalability and long sales cycles remain key challenges, making AM hardware startups less attractive to traditional venture capitalists accustomed to rapid software-style growth. Investors agreed that funding will increasingly favour companies that integrate AM into larger industrial ecosystems rather than pure-play AM machine manufacturers.

On the private equity side, the focus seems to be more on manufacturing capacity, i.e. contract manufacturing rather than Additive Manufacturing technologies. However, owners of contract manufacturing firms should be aware that the days of exiting with lofty valuations, like Stratasys’ acquisition of SolidConcepts in 2014, are behind us. Private equity investors are financial backers, not strategic acquirers; they are now prioritising lower multipliers with a focus on profitability. In the ‘Private Equity Perspective’ panel, Eugene Kim from AE Ventures focused on the need for “confidence in free-cash-flows.” At the same time, Mark Morrissette from North Atlantic Capital (previously mentioned) spoke about its focus on EBITDA-positive companies (targeting $1-10 million EBITDA companies).

Workforce development and skill shortages

One of the more pressing concerns discussed at AMS 2025 was the skills gap in AM. While AM positions itself as a solution to the manufacturing labour shortage (a true pain point), AM brings its own workforce development challenges. While adoption is growing, companies are struggling to find engineers, technicians, and designers with AM-specific expertise. From AM companies such as Materialise to users such as Mayo Clinic, the lack of qualified professionals was mentioned as a key factor slowing down adoption in many sectors.

Automation is emerging as a solution, especially in post-processing, where much of the labour burden lies. Advancements in automated depowdering, support removal, and finishing techniques will help scale AM adoption while reducing the dependency on skilled labour.

As AM grows, addressing workforce development will be just as critical as improving technology to ensure sustainable, long-term industry growth.

Sustainability in AM: expanding the conversation

Sustainability was widely discussed at AMS 2025. Specifically, Deutsche Bahn and BMW provided compelling case studies on how AM reduces material waste, lowers energy consumption, and enables decentralised manufacturing – all of which contribute to reducing emissions in supply chains.

Despite its potential, AM is not yet a primary sustainability driver in most industries, with cost and performance remaining the dominant considerations. For AM to be recognised as a sustainability leader, companies must clearly link AM adoption to measurable carbon reductions and supply chain resilience metrics.

AI’s role in AM: evolution, not revolution?

AI was another hot topic at AMS 2025 – with an emphasis on another. While software conferences are dominated by AI, the AM industry – by and large – perceives AI as an enabler rather than a disruptor. Panellists stressed that AI alone will not transform AM, but when paired with established workflows, it can streamline design, improve process efficiency, and reduce costs.

Among machine manufacturers, HP stood out for its focus on AI. It showcased AI-driven advancements that reduce design time from hours to minutes, cutting costs and improving part quality. HP highlighted AI’s role in sintering simulation and process development, demonstrating how machine learning models trained on past builds predict and resolve thermal anomalies before printing.

Several speakers warned against overhyping AI. Rather than positioning AI as a market differentiator, panellists advised AM companies to showcase how AI drives measurable cost savings, efficiency, and production reliability. The message: AI is a powerful enabler, not a silver bullet. Its real value lies in its ability to accelerate design, reduce waste, and optimise production workflows – but success depends on execution, not promises.

The road ahead for AM

The AMS 2025 conference made it clear that AM is transitioning from promise to proof. Across industries – defence, healthcare, automotive, and aerospace in particular – AM is no longer about disruption but about integration and impact.

While the industry continues to grapple with financial shortfalls and investor scepticism, there is still room for optimism. Narratives are shifting from technology-led to value-led. However, narratives alone will not suffice; investors are increasingly demanding more clearly defined paths to profitability, while customers expect more tangible outcomes and a better ROI.

Opportunities are clear, but execution is complex. Moving from a general-purpose machine sales model to a business model that aligns with customer value and customer success is hard, but several companies are starting to crack the code for this – and investors, in spite of high scepticism following the disappointment of the recent returns, are still willing to listen (and write cheques).

National security is a motivator but not a game-changer in itself. The American and European dependency on offshore manufacturing has been developing for decades, and it will not return overnight. Further, AM still has its challenges to overcome, from performance and reliability through standardisation to workforce development.

The key to success now lies in solving tangible problems, improving customer outcomes, and fully embedding AM into industrial ecosystems. As the industry matures, the focus must shift from flashy promises to delivering results. The future of AM will belong to those who integrate and execute, not those who rely on hype: integrate, don’t isolate.

Author

Tali Rosman

Business and M&A Advisor

RHH Advisory

[email protected]

www.rhh.group

linkedin.com/in/talirosman

LAST MONTH’S MOST-READ ARTICLES