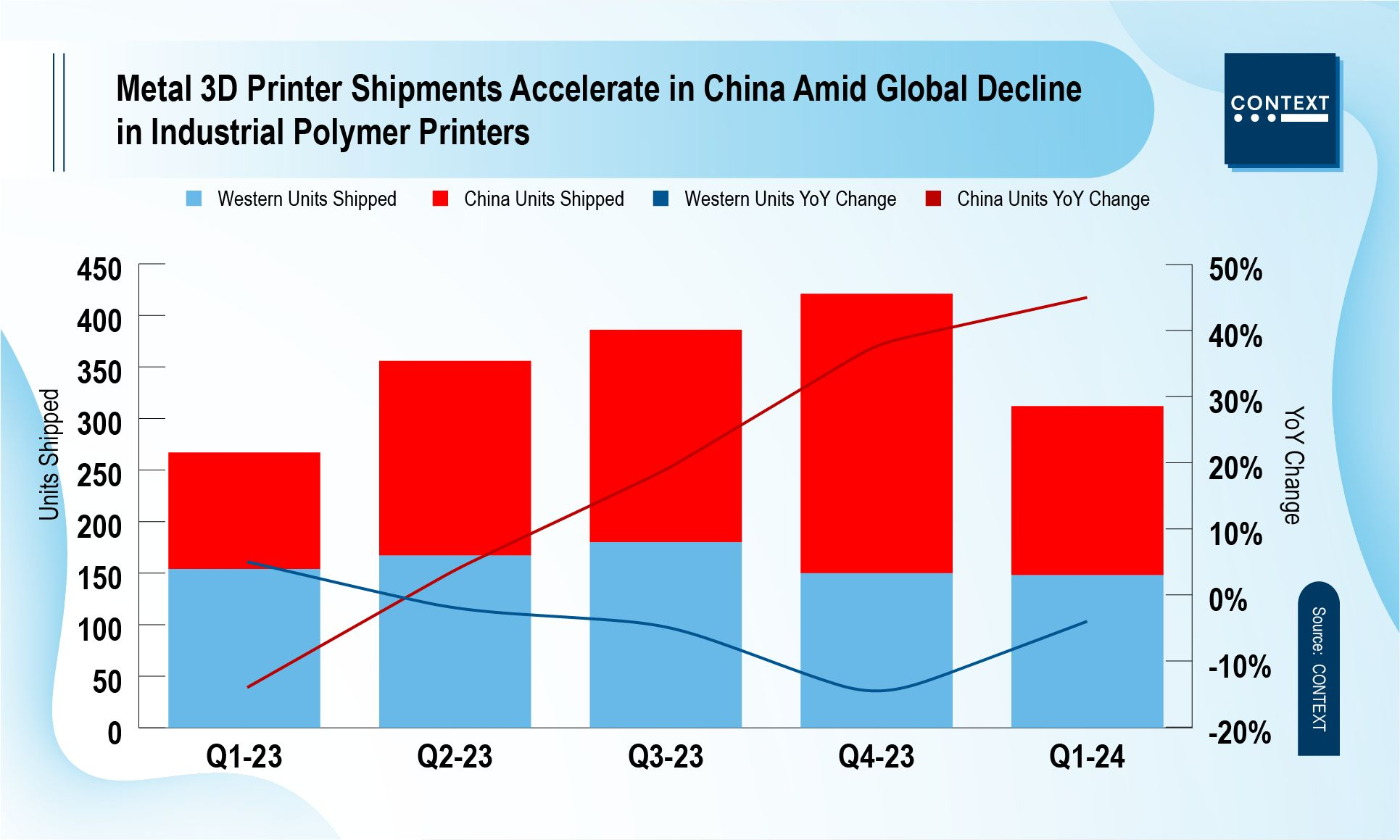

China sees surge in metal AM machine shipments, while polymer machine sales decline

Market intelligence and analytics company Context, headquartered in London, UK, has reported that global Additive Manufacturing machine shipments started the year at similar numbers to what was seen in the end of 2023. In Q1 24, industrial metal Additive Manufacturing machine shipments increased in China, while industrial polymer shipments faced challenges in all regions.

“Regional moods were divided amongst Chinese vendors – particularly those engaged in the industrial metal Powder Bed Fusion side of the industry – were elated by their strong domestic demand, while Western vendors noted continued end-market challenges associated with low CapEx spending due to high interest rates and sticky inflation,” said Chris Connery, global VP of analysis at Context.

“In the US and across Europe, the news was not all negative however, with many vendors reporting strong demand from domestic defence markets in the period.”

Industrial machines

In the first quarter of 2024, global shipments of all industrial-grade AM machines decreased by 15%; on a trailing twelve-month basis, they were down by 8%, according to the latest market insights from Context.

Polymer and metal machines together made up 96% of all industrial AM machine shipments during this period, with polymers accounting for 50% of the total shipments and metals accounting for 46%. Weak industrial polymer shipments were the main factor contributing to the overall decline in performance, with a 29% decrease in shipments compared to the previous year. In contrast, global industrial metal machine shipments increased by 10%. Looking at the trailing-twelve-month basis, worldwide industrial polymer machine shipments have decreased by 16%, while industrial metal shipments have increased by 4%.

Industrial metal machines

Shipments for industrial metal Additive Manufacturing machines across the globe in all modalities were up 10% year-over-year in the first quarter of 2024, with shipments for metal Powder Bed Fusion (PBF) machines — which accounted for the largest percentage of AM machines at 74% — up 7% from a year ago. Shipments of all metal modalities were up in the period with the exception of Material Jetting, with Directed Energy Deposition (DED) shipment up 21%, Material Extrusion (MEX) up 32%, and Binder Jetting up 15%.

Demand for industrial metal Powder Bed Fusion was particularly strong in China, with shipments from Chinese vendors up 45% in the period, while shipments of metal PBF machines from Western vendors were down 4% from a year ago. Chinese vendors have seen year-over-year quarterly shipments grow the last four consecutive quarters, while Western vendors have seen four consecutive quarters of declining shipments.

Four of the top five global vendors for industrial metal Powder Bed Fusion AM machine shipments in the period (Eplus3D, BLT, ZRapid Tech and Farsoon) were headquartered in China, with Eplus3D leading the industry in the period. Vendors focused on the West continue to lead in System Revenue contribution, with Nikon SLM Solutions and EOS enjoying the top market share positions in metal PBF machine revenues in the period. Nikon SLM Solutions was particularly notable as the leader in large form-factor, multi-laser machines.

Outlook

“Talks of industry consolidation dominated the recent conversations in the West, highlighted by Nano Dimension’s planned acquisition of Desktop Metal,” said Connery. “Ongoing merger and acquisition rumours persist in the US and Europe, with several publicly traded companies under strategic review. In contrast, Chinese companies continue to thrive domestically and focus on expanding their overseas business.”

Western forecasts remain conservative, but strong Chinese demand — especially for metal Powder Bed Fusion solutions — has led to a revised global industrial AM machine shipment forecast, now projected to rise by 7% in 2024. Western defence sector demand from companies like Nexa3D and Velo3D also supports this increase.

“Accelerated growth in the industrial price class is anticipated in 2025 and beyond as the US and Europe stabilise post-election cycles and interest rates drop,” Connery continued.

“While system vendors remain focused on further advancing Additive Manufacturing into mainstream manufacturing, many strategic growth initiates are now starting to also incorporate other digital production technologies beyond just additive into their portfolios, as a way to accelerate growth.”